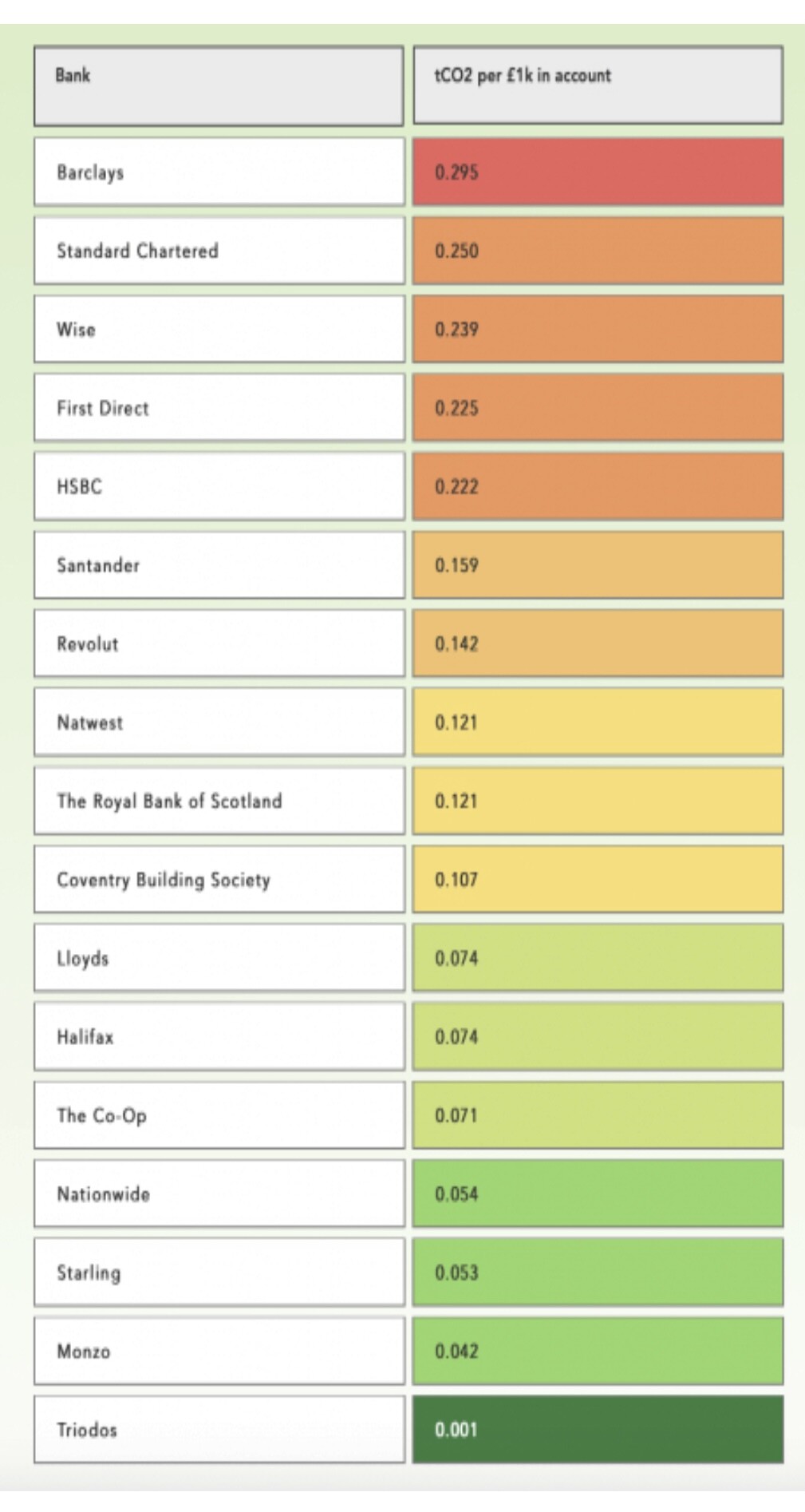

Thought some may find this interesting. Some takeaways:

Triodos lower than all by a distance - making them a good place to leave deposits if this is an important issue to you.

Interesting to see e-money licensed banks high - perhaps as your deposits actually sit with the likes of Barclays (Wise do use a Barclays sort code)

Interesting to see one Building Society lower than another (Nationwide to Coventry). Generally interesting that Nationwide are so low given their reach.

Interesting to see Lloyds etc not a great deal higher than the Coop who market as being environmentally friendly (despite them still being on the lower end).

Monzo and Starling low, presumably due to not lending or investing a lot generally speaking?

Barclays & HSBC well out in the lead in the “dirty” stakes.

“Each £1,000 held in a current account could be considered responsible for contributing up to 0.29 tonnes of carbon per year, if you hold your money with the worst ranked offender Barclays – the equivalent of driving over 729 miles in the average passenger vehicle.“

Yeah, I’d like the context around how these numbers are produced too. Monzo being that close to Triodos surprises me, so it’s surely not taking into account the bank’s own operating emissions.

Oh I wasn’t questioning Triodos’s score. I don’t doubt it. But I don’t think Monzo’s would be that low if it wasn’t heavily focused on where the bank is investing deposits. Same for Starling.

I don’t envy the task of trying to grade them. Unless you’re as transparent as Triodos, and none are, you just don’t really have all the data to measure it properly. And even then, it’s not a simple calculation.

I think that’s why a lot of places just resort to judging them based on how much money they pump into fossil fuels.

One thing that matters to me as well is the bank’s own emissions, and even the neobanks aren’t as clean as they should be there, considering they’re all digital.

Like all tools like this, it’s a really good glanceable guide if you’re just wanting to make a quick decision.

I think, personally, the main merit is to draw the attention of people who bank with the likes of Barclays to the fact that there may be a reason to evaluate things (if you consider it an issue of importance).

The main thing to watch is savings providers that keep your savings at a 3rd party bank --NS&I, Principality etc. The latter keep your savings in a Barclays account, putting them at the top of the CO2 table. I believe NS&I is NatWest, so mid-table.

I also wonder if this list is separating retail banking from investment banking --Lloyds retail banking may be relatively clean, but their investment banking arm probably isn’t.

If when you transfer money to your wise or Coventry account you use a name other than your own for the confirmation of payee, chances are it is a 3rd party holding the money. With Principality and NS&I it is their bank account but your holder’s number.

I had a look on the Coventry website. It says when setting up a standing order:

Coventry Building Society

Sort code: 40-63-01

Account number: Use the last eight digits of your account number.

So, your money is held with HSBC by the look of it. Wise is just an emoney account like Chip. It is held who knows where.

Ring-fenced funds can’t be invested so Wise etc shouldn’t matter what underlying bank is holding the deposit.

I’d also probably wager @Rexx that the majority of people don’t care about how many carbon emissions are generated from their holding £X in Barclays; people have bigger problems and the ones who don’t, are moving pence, not pounds.

They’ll all sit on top of cloud platforms and MC/Visa physical infrastructure that needs to be plugged into; it’s not possible to move these into entirely carbon friendly things

The lack of branches probably just means they’ve got a lot more difficult a job of making reductions to their emissions

I don’t think either of them are significantly lending, to be fair. They’re probably making more money from BoE right now than any other avenues.

Never before have I seen a website for less people. Innovation is great, but the innovation needs to be better enough to overcome inertia. Being low carbon isn’t going to switch the vast (and I mean nearly 100%) majority

Would be a bad way of calculating since Barclays can’t access the funds; I’m guessing it’s probably because Wise has investment features and WRT Revolut they’ve got actual savings accounts with partner banking institutions.

They do - but Allica currently score quite well (who my vaults are with) so I guess it depends? I think Investec are another partner bank

You are probably right about ring fenced funds - I think it comes back to what others have said about more detail on how the numbers are derived.

As for people not caring about the environmental impact of their money - I think it’s useful to make people aware of how banks actually use deposits - people can then make their own minds up (I also think people should care but that’s just my opinion).

And yes I think investing in new low carbon infrastructure is more important than just being low carbon - due to the way investment works in economic terms. Again more detail on whether that affected the numbers would be good.

This is a gross misrepresentation of how Building Societies work. They use your funds to lend to other customers, they only use those banks for clearing, i.e. getting your money from you and returning your money to you.

They’re not just a frontend for a bank, like Chip, Plum, Revolut, Moneybox etc.