I don’t think they do, but I have only ever used Santander as I read about the tip on the MSE forum (I think it was) before I got the account.

Revolut should also be OK.

The good thing about SEPA Instant is that 1) Fineco have it in case you ever really need it in an emergency and 2) Since they support it, if somebody else sends you money via SEPA Instant you get it instantly (and, I think, for free as they only charge for outgoing payments?).

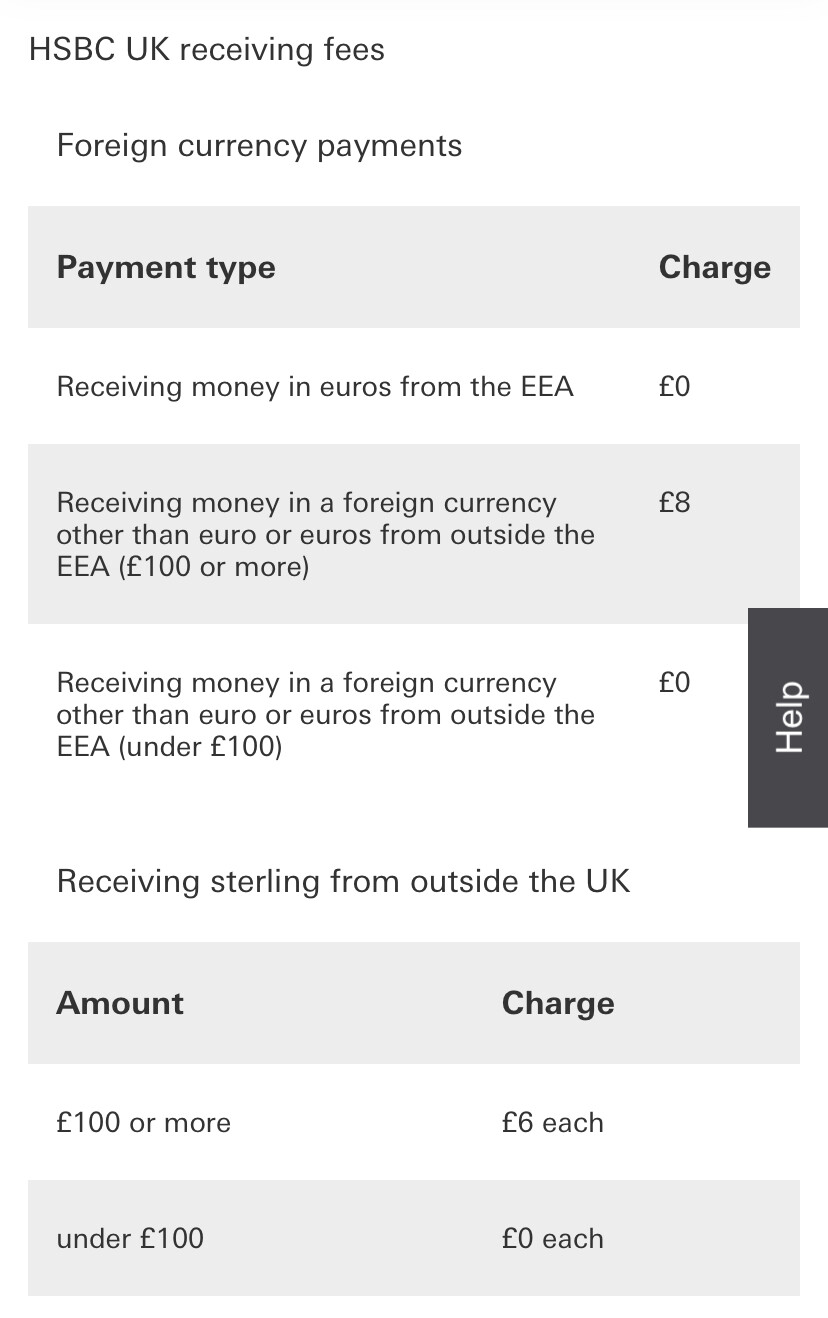

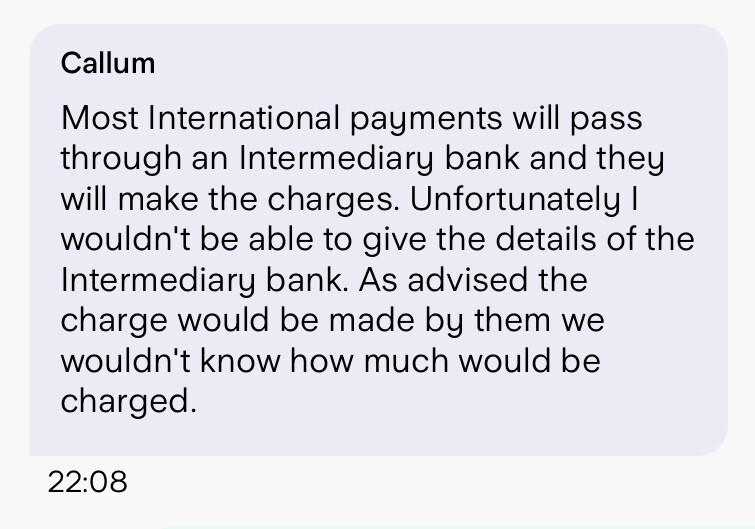

Ah, the chat advisor has just wanted me about the potential for intermediary bank fees when receiving via SWIFT. With Starling being such a small bank without the kind of international/partnership network that a bank like HSBC has, do you think these are likely to be an issue, even for just GBP transfers?

No, I think the payments pass through Fineco’s larger Italian parent UniCredit, possibly Lloyds (who seem to provide Fineco’s U.K. sort code) and maybe NatWest (for Starling, I know they provide some services for them) but I think fees for a GBP payment would be unlikely. There must be no fees at least until the end of the Fineco-related chain as otherwise I would have seen Santander charge.

They are right to raise it though, and there is no way to really know without trying it.

As a general rule, your payment would pass through more intermediaries and there would be a higher likelihood of them charging if it was sent from a country with a totally different currency to an account with another different currency further away.

No. They accepted an application that had a minor error in it, that almost every other system would either have flagged up (to me) or allowed it

“I’ve never needed to contact their support as I’ve never had an issue”

But then you pass judgement on the Customer Service function, even though you’ve never used it

"do you really need support all the time? "

No. But if I ask a question about something, I would expect someone to answer the question I asked. I asked how to input the number of a card I didn’t have. They didn’t answer that question. At all.

“Are you sure that the 8 digits they were asking for were not either 1) your account number or 2) one of the Fineco passwords/PINs to confirm the request?”

Absolutely. Infact they just confirmed to me that I couldn’t request a card because I didn’t have one. They have manually ordered one for me.

I didn’t pass judgement on the customer service, I simply talked about my experience with bunq and suggested that I’d be happy with Fineco’s service if it was similar, or even slightly worse.

I suggested that, pragmatically speaking, if Fineco are offering something nobody else is, I would be happy with the trade-off of potentially not-great support; given that they are operating from an non-English speaking country I wouldn’t have such high standards as I would from a British high street bank, and wouldn’t necessarily expect excellent service if it’s a mostly self-service online account - which it is.

I would still expect basic competence, obviously, and maybe you got unlucky with getting a less good support agent.

You also seem to have issues with bunq now - again, what is the problem with them pasting a response to me if it addresses my question? None, I would suggest.

I stand by everything I’ve said and, if Fineco isn’t for you, you are welcome to continue using Wise/Starling/Revolut either on their own or in some combination. Choice is out there!

I would, but my Apple Pay is full from having already added the maximum number of cards, and I can’t be bothered to remove and re-add one of them just for that.

You can open an account at finecobank.co.uk but there is currently an account opening offer which you may be interested in if you think you might want to use the trading side of the product (it’s 100 free trades for both you and the person who refers you by using a “friend code”).

I’ll try to find out how to get a Friend Code, but it’s not too obvious from having a quick look!

The Apple Pay limit is due to the Secure Element of the devices only being able to store a limited amount of data. Originally, the limit was 8 cards, then it was increased to 12 for A11 devices and above. Now, with iOS 15, it seems to have increased to 16 but I’m not sure how they’ve managed it!

Yep, I think Euro is definitely the sensible way to go, as much as I want to be able to use a pretty all black card day to day at home! I’d be very tempted to pay the £10 if the app was Monzo/Starling tier, but it seems quite a way off from that so I just can’t justify it when I have such great options from other banks at my disposal and totally for free.

@Seb out of interest, is the BIN of your Euro card Italian to match the account IBAN, or is the card UK registered?