The police were called too. It’s the shameful lack of responsibility on her part that gets me. She blames the bank even though they got the authorities involved. This process causes so much friction with banking customers yet you have someone who outrightly ignores it. I’d love to know what she thinks the bank could have done differently.

FOS have a lot to answer for here too.

Even after a low friction electronic warning FOS have said the warning has not been understood by the victim so the bank must refund.

I’m not in the game of protecting banks but retail banking cannot be free forever in the UK if this is the cost to banks.

Honestly, the only option will be for banks to stop online payments completely and ask people to go in branch with evidence to make a payment

If the big red warnings repeatedly shoved into your face aren’t enough, then nothing will – might as well not have them so the everyday user isn’t inconvenienced. Anyone who falls victim would do so anyway

Yes, this was being discussed over on the Monzo Community a while ago and I advocated exactly that.

Apparently even when the code has been followed, in some cases the Ombudsman has forced the bank to pay-up in a “no-fault” capacity as the specific circumstances of the scam made it “believable” and “seem authentic”!

The banks really cannot win, and meanwhile it’s becoming nearly impossible to make a genuine payment without irritating hoops to jump through and warnings in your face; scammers are cleaning banks out and we all (through higher charges, lower benefits, etc) are paying for it.

There has to be an element of people taking responsibility for their own actions. They might be stupid, but there is no regulatory obligation on banks to “protect” the stupid and nor should there be!

One thing out of this story that did stand out, was the way the actual fraud was initiated. It seems from reading, that the scammer obtained a replacement driving licence for the homeowner and that the licence was sent to the victims home owner’s address where he clearly still had his driving licence registered at but he wasn’t actually living there and hadn’t it seems, for quite some time. Isn’t that kind of setting one’s self up for problems even if it’s an oversight or unintentional?

I wonder just how many people who rent out their homes long term but live elsewhere do exactly the same thing? To me, personally, it just doesn’t make sense to not change your DL address to the place you’re actually living at. People however, will always have an excuse somewhere not to do the sensible or most appropriate thing.

I have to admit, I’m absolutely stunned at the amount of searches that have been carried out on my new build development, or perhaps I shouldn’t be, after all, it is a new build development!

So basically after registering for an account and following a telephone conversation with HM Land Registry, my actual home is still in a queue for the Title to be registered on their site. This apparently is absolutely normal and eventually, my conveyancer who completed the house purchase, should forward the Title Deeds either to me, or more likely, my mortgage provider. In the meantime, the actual development land that my home sits on, every single search that is carried out, I will receive an alert for, so there’s this huge list of mortgage providers, solicitors/conveyancers who have all carried out their searches since the development was started.

No proper details within the article for clear context of the scam though, other than “transferring the funds to scammers in the United Arab Emirates”, and cba to search for it tbh.

It’s a pretty short reading by the Supreme Court, but worth to read, imo. Barclays are in the right. 700,000? You should be seeking counsel on that kind of arrangement. Your bank isn’t your lawyer.

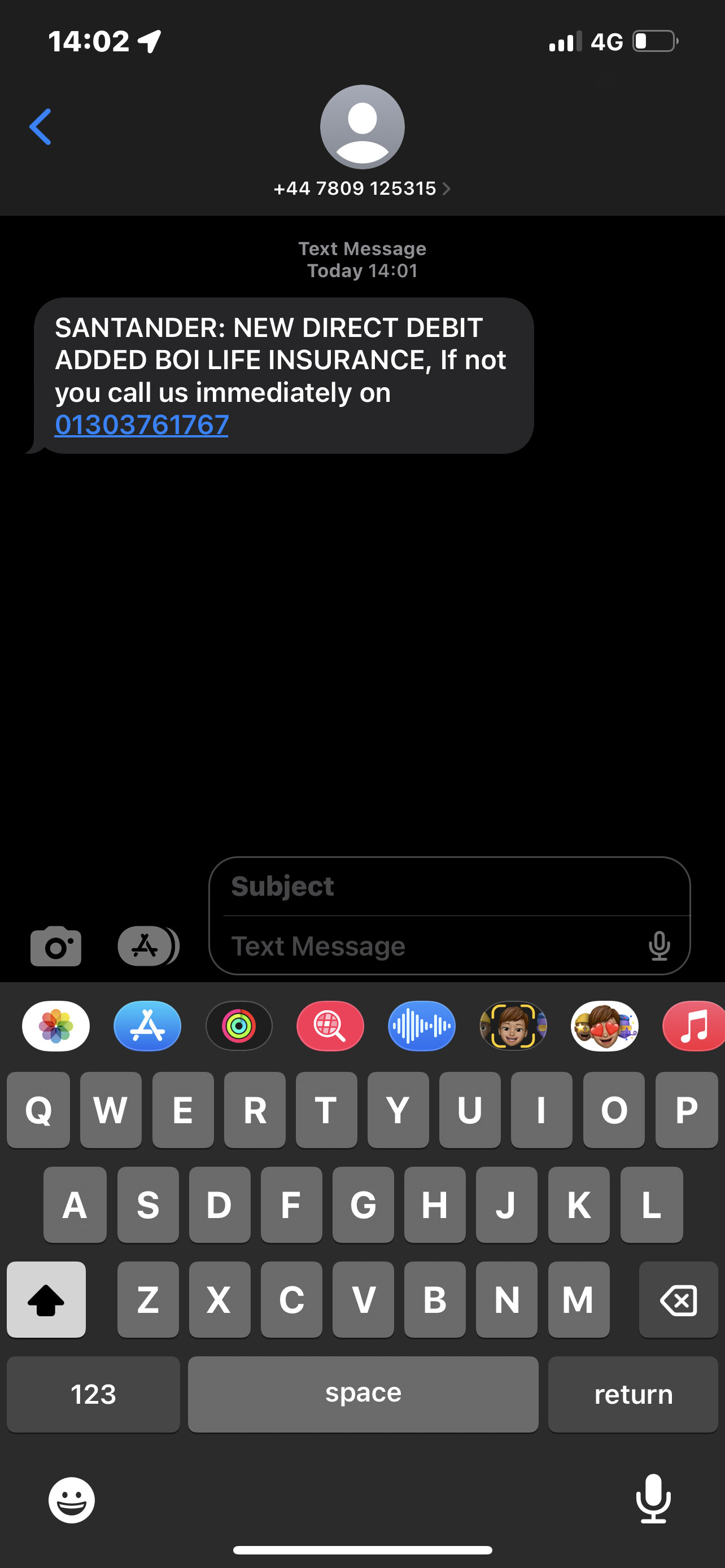

The thing with these type of scams is everyone can be caught out if they catch you at the right time. May look obvious, but lots of people fall for them. If they catch you when you’re stressed, tired, you’ve just had some bad news, etc., the odds go up that you may not react how you normally would. If they send a million messages about “your Capital One credit card account”, anyone without one will immediately dismiss it. However, the Capital One customers in the list might bite.

In theory I could scam you out of a tenner at a local pub… does the bank have to intervene then? They carry out instructions - if you want an account where they scrutinise your every move, sign a power of attorney and then have someone scrutinise it for you

Banks have a duty to help vulnerable customers, so informing a bank is probably helpful to them to see if they need to place any arrangements around your spending (i.e. maybe you have a gambling addiction and want to make an arrangement for an irremovable gambling block / ban on cashpoint withdrawals)

but also, they can’t be liable for simple stupidity… how could we implement such a shift in responsibility? the end result would be moving your money around would become a multi-step multi-day process with you going into Post Office Banking Hubs to sign documents and have in-depth discussions with staff…

That’s the thing… it’s not stupidity. It’s innocent people being caught out by often very clever scammers who know exactly how to socially engineer people. I feel sorry for anyone who falls for this type of scam. We’ve had customers send thousands of pounds to a scammer’s bank account because their email account had been compromised, and the scammer intercepted and doctored an email requesting the balance be paid before their new vehicle is delivered.

Even if you say it isn’t stupidity, ignoring that point entirely: the bank doesn’t become negligent to the point of having a liability

Sometimes there are mistakes we made, like my friend with FTX. Lost $8000. Yet he had no recourse bar submitting a claim as part of their bankruptcy proceedings.