Just asking for some advice if any one can help. Monzo have registered a default on my credit file. I switched the account months ago, and I had an unarranged overdraft remaining on the account. Admittedly, life events and other things got in the way and I genuinely forgot about it which is an error on my part.

I received an email to get in touch before a certain date with an offer of repayment to prevent a default. I replied immediately upon receipt of this email with an offer of repayment. However, I never received a response to this email and they subsequently registered a default on my credit file.

I emailed a complaint about this, but they’ve responded today stating they’re not upholding the complaint, and that there is no record on their system of me getting in touch with them. However, I have the email in my sent email folder with the precise date and time, and it was before the deadline they had given which they said would prevent a default being registered.

I’ve asked them to look at this again. If I get no further with them, would the financial ombudsman help with this?

Have you shown them the email you sent? With the correct date and time stamp? Have you forwarded or attached the email including all headers so they can verify it?

If you haven’t, do that.

Yes, take them to the ombudsman. Don’t expect that to be a quick process though. I’ve been waiting over 8 months and still don’t have a case handler for my complaint against Monzo yet.

i) whether the company has broken the law (this is extremely rare)

ii) whether the company has followed its own terms and conditions in dealing with you.

Given the laxity of the latter, finding for yourself is less likely than you would think

I took the time to read this explanatory stuff from the Ombudman’s Office. Impressed at just how readable this is - clearly drafted with the customer in mind.

It’s reassuring to note that the FOS doesn’t expect all the “t’s” to be crossed when submitting a case.

Very true. Sainsbury’s did technically follow all the letters of the law with me.

The FoS considers a lot and pays out quite well when it deems the bank to not be acting in the spirit of customer service.

I read a story even, where they required a bank to refund a man in a pub that spent about a thousand or so organically and then had his card swiped, because they thought that (even though the card was used regularly for daily spending) that it was unusual and reasonable to expect that if a payment fails and is retried several times in a row with lower amounts, that the bank should be aware this could be fraud.

It’s definitely a good service in considering the “regardless of the law: does X sound like it lines up with common sense and reasonable conduct? if a person on the street heard about X, would they immediately go ‘wow that bank is disgusting in their conduct’”

Sent the complaint to the Financial Ombudsman and their initial investigator has upheld the complaint and ordered Monzo to remove the default from my account, arrange to have the overdraft amount repaid and to pay me £100 compensation.

Monzo have now said they don’t agree with the outcome. So I assume it’ll go to a full ombudsman now then. What a disgrace of a company they truly are. So much for empty platitudes of building the ‘best bank in the world’ and ‘making banking easier’. Never being treated so appallingly by a bank and attempting to penalise me for their own incompetence. So thankful to be at Starling who are light years ahead of those idiots.

Pretty quick turn around from the ombudsman. They must be getting their act together. I think it took them a good 8 months just to get around to dealing with mine.

Sadly it wasn’t the full ombudsman report. When you refer to the financial ombudsman, they assign your case to an initial investigator case handler who looks at your complaint and decides whether to uphold or not uphold the complaint. They then attempt to resolve it in the first instance. Monzo have rejected their findings and now it will likely be sent to an actual ombudsman and that will take many months to get looked at.

Yeah, thats what I had to wait all those months for. They upheld my complaint and Monzo agreed with my decision so it was all settled a few months ago. Otherwise I’d now be waiting for the ombudsman like you. I since reported them to the FCA as well over the issue I had.

What effect does something like this have for Monzo? Are there any repercussions for them, other than having to spend the time and pay any compensation?

They’ll be expected to adjust their processes in order to prevent a repeat occurring to other customers in future. Ultimately they can refer the matter to the FCS if they judge the bank to be in breach but that’s unlikely.

Worth considering that every FOS complaint costs Monzo somewhere in the region of £750, so they are incentivised to settle complaints themselves.

Just costs them time and money AFAIK. Probably repetitional harm too, which might be why they tend to fight them so aggressively.

The FOS, as they explained to me with my complaint, can only consider how you were treated but can’t actually force the bank to change how they do things, as that’s a matter for the FCA. They can’t (won’t) refer something to the FCA themselves but in my case did recommend I do so in their decision.

The FCA are the ones with the power to actually make them change a process, but they’ll never tell you of any action that comes from your complaint, but in my case they did agree Monzo were acting against regulations with their clock processes in terms of overdrafts and forwarded it to the team who supervise Monzo. That’s the last I’ll ever hear on that. Time will tell if Monzo fix it, and if they do I’ll never know if it was the result of my complaint or not.

They’ve already built a solution for the US branch, and so could just port it over and say they were always going to.

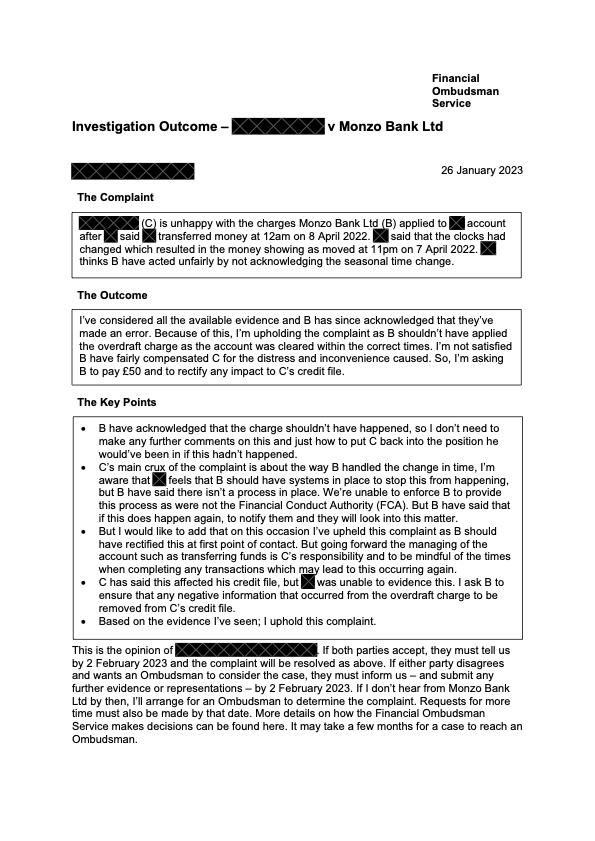

Here’s my outcome. The brunt of my complaint related to their whole clocks process, which they weren’t able do anything about besides compensate me for the issue that transpired as a result of it.