I’m curious If anyone uses P2P as a form of investing?

I used Elfin Market a while ago for borrowing and was really impressed. Actually one of the most impressive fintechs I’ve ever used.

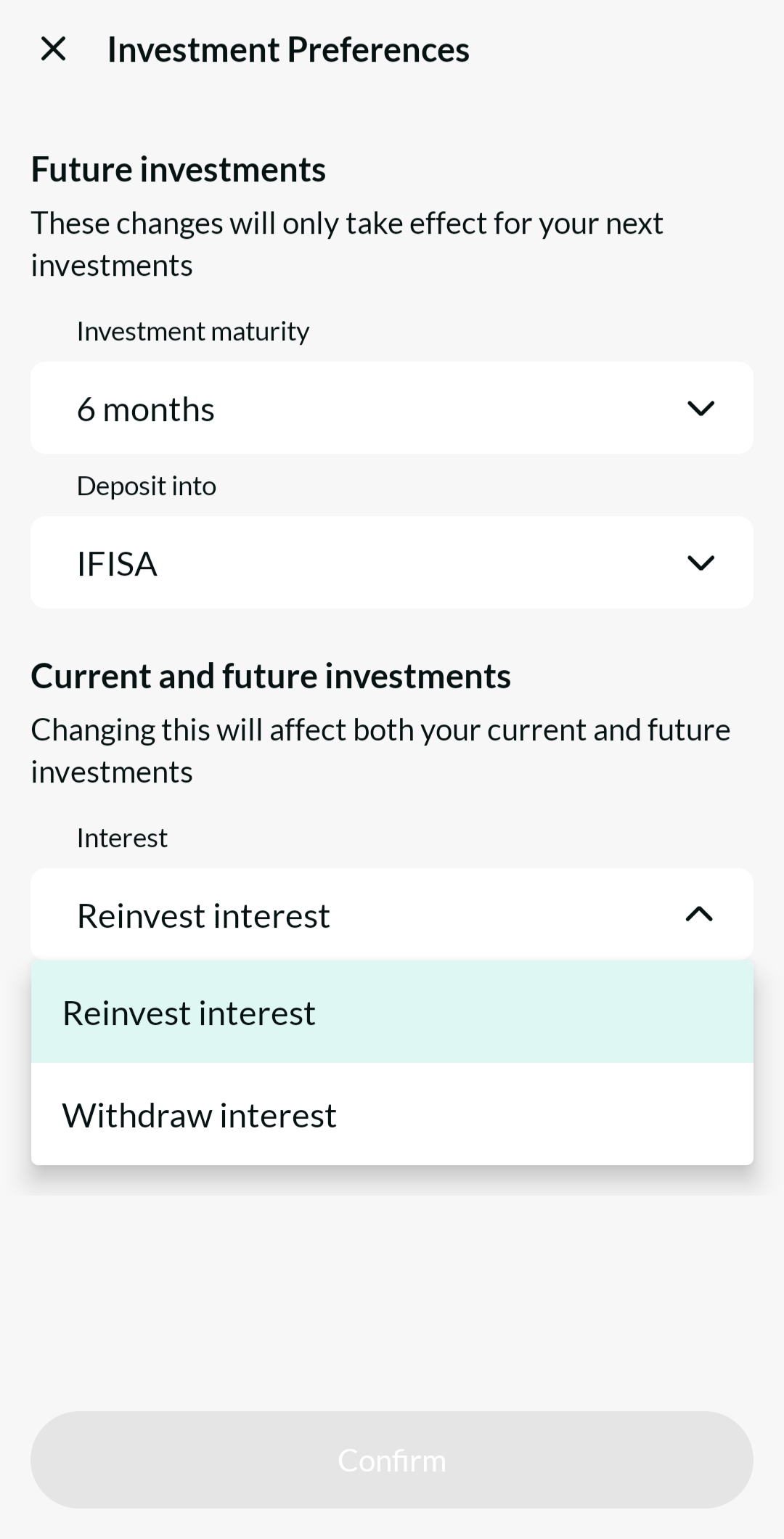

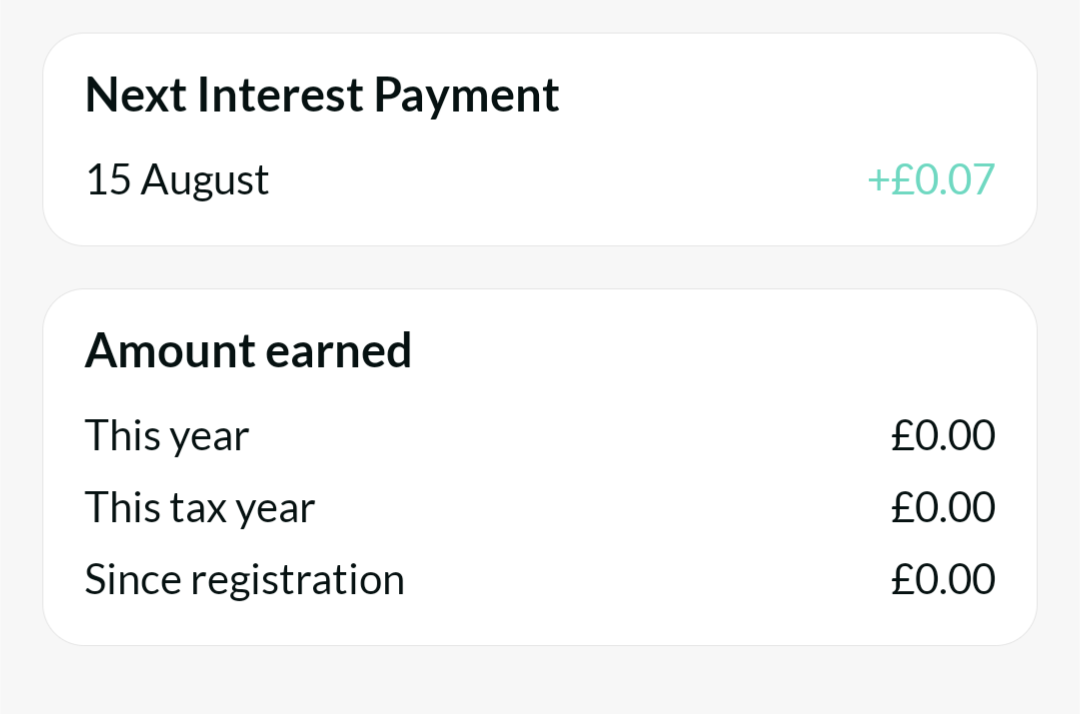

I’ve set up an innovative finance isa with them now out of curiosity and it’s all been straightforward so far. They said that money is lent out in usually 1-3 days but anything I’ve put in so far has been less than 24 hours.

Far too risky, IMO. You are completely dependant on borrowers actually paying back the funds which are loaned to them. If they don’t, you lose that capital.

I saw that and dismissed it straight away. A S&S ISA can contain anything from very low risk to very high risk investments, so the comparison makes no sense.

This basically. Them saying this is a bit like buying a car off a guy with a whippet down the local pub, which is “definitely not stolen”.

I don’t know how they can get away with saying they are comparable, when they really are not. Personally not for me, I wouldn’t be sure I’d ever see the money back.

I had a few thousand invested across about 10 p2p platforms in the late 2010s early 20s. It was risky but fairly profitable. Most of them have gone into administration or moved out of p2p (ratesetter, zopa, funding circle, assets capital, growth street, ablrate, mintos, archover, and a few others). Lendy and collateral were a disaster but i never put any money in those, the others turned a profit despite them being a complete shambles during COVID. I lost money in ablrate, which I suspect might see some legal action against it from the lenders at some point for reasons. Diversification was essential back then, and I’m not sure there are enough providers for that these days. The only one I’m still invested in (to a minor extent) is unbolted, which just plods along. Loanpad seems to still be doing ok as well, and I never liked elfin’s business model. There’s a decent p2p forum which has a lot of info, although that’s almost dead now too.

Too much hassle and risk for the return these days, when savings can net you 6%, I pulled out almost entirely in 2020, was a bit of fun while it lasted, but the lack of regulation made it very much the wild west of investing.

For me the issue with P2P lending is liquidity. I don’t think I’ve lost any money overall (in the sense that overall I’ll get out more than I put in), but I have experienced issues where I’ve had to wait to get access to my money because platforms chose to pause withdrawals (particularly during COVID) or because of lack of demand from buyers on secondary loan markets.

Yes, it’s supposedly regulated by the FCA, but in reality they’ve had absolutely no clue how to handle P2P from the beginning, there might still be profit to be made, but for me personally it’s no longer worth the risk of substantial losses for an extra 1 or 2 pct over a very safe 6% in savings.