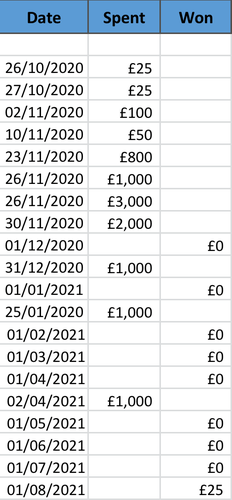

With Premium Bonds, you should expect to win around £100 a year if you hold £15,000 worth. Obviously, there will be years when you win more or less than that.

Last year I realised a return of 0.97% on my Premium Bonds holding.

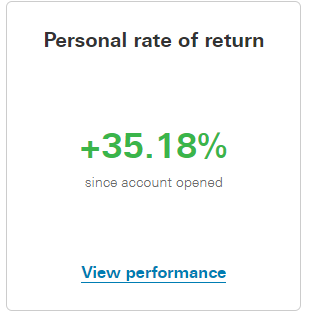

In contrast, in five months this tax year, my S&S ISA is currently showing a near 8% return, on a third of the value of my PBs.

My PBs? 0.35%

This is my first year of investing, rather than saving. Perhaps if I had done it earlier, I may have had better returns over my lifetime. Very risk averse though, me

You can’t compare an investment account with a minimal-risk account (such as premium bonds or cash savings).

They (should) have completely different roles in wealth management.

Risk is all relative. I’m probably the biggest risk to my savings, but after that it’s inflation so I keep the bare minimum in cash or equivalents. If I need more than that I can sell some shares in a few days, but I’m reluctant to do that unless I’m desperate.

It should also be noted that you can keep cash, or invest in bonds funds in an investment account, it’s not all lairy, seat-of-the-pants stuff.

Not really. Clearly investments carry a higher risk than savings. I’ve dabbled in investing before so it’s not all new to me, but decided that ultimately my emergency fund is safer in PBs than invested. What if there’s a market crash and you also lose your job?

If there is a market crash, similar to that of the great depression, then chances are the cash tied up in an emergency fund won’t do a great deal either. During the great depression, CPI was between 13% and 18%.

However, during the Depression, stocks dropped but eventually recovered. In 2008 they did the same…and again at the beginning of the pandemic. Don’t get me wrong, I have cash on the side for when fund shares go on sale, but I keep my outgoings low and even if they dropped 75% I’d be ok with the cash I have.

Whilst cash yields basically nothing, but inflation is still relatively high, cash is far from risk-free.

Those stocks drop in value though which is the risk. High risk investments are risky because in a downturn their value might have significantly dropped or the companies could have gone bust leaving you with nothing at all. where as while spending power may have gone down, your low risk premium bonds (in this instance) would not have disappeared.

Having your emergency funds in high risk ESG funds is a potential disaster waiting to happen, especially with no cash reserve.