![]()

I have been wondering why this group hasn’t been picked up by the media before now.

It’s a shame that the article doesn’t mention what proportion of those complaints were upheld.

If memory servers from when I looked through the ombudsman’s website, not many complaints are upheld.

1 Like

I recently retired and received a 6-figure pension lump sum into my Starling account. I then proceeded to send large amounts to various savings and investment accounts, plus some smaller amounts to family. I had been a bit concerned about how Starling might react but haven’t had any issues at all.

The lump sum came from a well-known pension company and most of the outgoing transfers were also to well-known companies, so perhaps this is why I was OK.

Contrast this with HSBC whose Fraud department called me after West Yorkshire County Council credited my account with a 4-figure pension lump sum which I had then tried to transfer to Marcus. They blocked the payment and gave me a grilling about where it was from and where it was going, constantly telling me that it looked suspicious!

This is why, when chasing the best interest rates, I tend to move savings through Starling rather than HSBC.

I was also unhappy that HSBC would call out of the blue on these occasions and start asking for personal information, including debit card number, expiry date and CVV. This from their fraud section, too! To be fair, they appear to have improved things a bit recently by now sending a text asking you to call them regarding your transaction of £N.

1 Like

I had a six figure pension lump sum a couple of years ago and, tbh, wasn’t prepared to gamble with either my Monzo or Starling accounts, and the daily limits imposed as well.

Used Nationwide and spread the funds out within 48 hours, with zero issues.

for the legacy bank

for the legacy bank

2 Likes

I’ve long had a theory on this topic, which is totally out of thin air and with no knowledge to support it, but which I believe is probably true.

My thoughts are that with Fintechs, the whole USP is that you can get up and running with a new account quickly and easily (and without attending a branch or posting documents); therefore customer ID and anti-fraud checks at the outset must be relatively light-touch. They then have a lower overall confidence level that you are a “genuine customer”, so future transactions are treated with more caution - in other words, you are likely to need further Know Your Customer and Anti Money Laundering checks if you want to do anything “out of the ordinary” later on, overall limits on account activity will be more restrictive, etc.

This is a deliberate business strategy for the Fintechs; simply do less checking up front to make account opening easier, reserve further KYC/AML for later if required. Some customers will never need extra checks, but probably more customers as a proportion of the entire customer base will. Some will also fail these checks, for some reason or another. You will then see a slightly higher than industry average rate of account closures.

As I say, I can’t prove it but I suspect that is what is happening.

3 Likes

E-money institutions may be able to get away with slightly less, but all banks have to adhere to the same set of rules regardless of how they operate. Now whether all of them stick to the bare minimum; or if the traditionals (or maybe the fintechs?) go above and beyond, we’ll never know

2 Likes

I think they all do the bare minimum, as fintechs, often only asking for one proof of ID and not a separate proof of address (which I have usually needed when opening an account in person in a branch, for example).

I also have other theories related to this: fintechs are less willing to swallow fraud losses so they would rather freeze or close a dodgy account than keep it open (I think they are probably more trigger happy, as they are also aware that their accounts are easy to open and will therefore be a magnet for would-be fraudsters).

Regulators also probably give the big incumbent banks a bit more slack than equivalent fintechs, so again the fintechs have to be more careful as they are under greater scrutiny. They therefore err on the side of closing or freezing accounts where the same activity may have gone under the radar of big banks (I’m thinking here of things that aren’t actually illegal, just potentially suspicious - like crypto trading).

3 Likes

I don’t know if that’s right, but it makes a whole lot of sense.

2 Likes

Thanks, at least my theories don’t sound completely implausible.

It just strikes me that you have a low bar to entry (which, although clearly in accordance with FCA guidelines, may be slightly less than rigorous) and a seemingly high level of reports of account trouble (from fintechs in general really, but most famously Monzo perhaps as a result of their prepaid origins - as implied by Chris Skinner).

It doesn’t seem like too much of a leap to suggest that the low bar to get in has a trade-off in an attitude of high sensitivity to risk; playing out in closures and so on.

1 Like

Much like the Chris skinner articles that have come out over the last week that have been formed by correlating user reports with his industry experience, I think it’s a pretty solid theory that the prominence of these issues stem from something out of the KYC/AML process.

Whilst it’s possible everyone is just lying, and they’ve actually been doing stuff they haven’t, I don’t personally see those people kicking up that much of a fuss. It feels counter intuitive to me to bring attention to something where you’ve done something wrong and wouldn’t want everyone finding out.

I already know from my experiences that quite a few fintechs did not gather all the information they required of me during the onboarding process to fulfil their regulatory obligations. So not only does KYC/AML seem like a plausible explanation, it seems likely too.

Of course it’s speculation though until if/when regulators decide to name and shame, like BaFin have done to N26. N26 have been in the game longer than our players and have more experience. They’ve made mistakes, and it’s fair to assume other fintechs have made similar ones too. N26 fell foul of U.K. regulations a few times during their time here, but I don’t recall those being publicised by the regulator besides a few journalists in fintech picking up on them.

That’s the thing - if they actually were criminals, they wouldn’t be approaching the Guardian or whoever to get their case investigated!

When you read the stories, sometimes it is pretty obvious that something happened (either they have lied by omission, or used their account for business purposes, etc, in contravention of the terms) but I feel that it would be unlikely to explain everybody who has had trouble.

1 Like

The more I consider it…… yep, that just fits. Bit shabby though, eh?

As an aside, this very area of uncertainty that you describe is the very reason I reluctantly moved from a fintech bank as a primary bank. I just couldn’t countenance being faced with closure (I tend to fully commit with my banking affairs).

That level of doubt just doesn’t exist with (a good) legacy bank.

1 Like

I don’t know if you saw the response on the Monzo forum to the Chris Skinner article from Simon(Ex-Monzo for those who aren’t from that forum), I’ll post it below just in case but its worth a read, gives a small insight

I’m going to go out on a limb and say he’s wrong. Firstly, I dispute that our KYC was ever lacking due diligence, although I won’t go into the details of how it worked for obvious reasons. But even if that was the case, in June 2017 there were heavier additional measures put in place to comply with EU AML regulation. At that time, the prepaid beta had some 250k accounts. Let’s say that 80% of those people are still Monzo customers today, so 200k people. That’s only 4% of the userbase. When you account for 30 day actives and you remove the people that barely use their accounts and thus don’t even have enough usage for there to be a chance of suspicious behaviour, you’re probably lower than 2%.

And from time I spent working on fincrime-adjacent tasks, I’d have to say there’s absolutely no chance in hell that even 50% of the accounts flagged were people who had been customers in the prepaid era. It was far, far less than that.

It reads like a plausible theory to an outsider. It’s not a plausible theory to me.

I firmly do not believe that Monzo closes or freezes more accounts than any other bank. What I do believe is that, as an app-based bank, these customers are far more social media savvy and far more likely to join such a group or kick up a stink on Twitter, compared to, say, somebody that got their account frozen with Barclays or HSBC.

1 Like

I feel the same, and if I remember rightly you moved your affairs to Lloyds as a primary account?

I’ve been using Bank of Scotland (a similar good app), purely because they pay an OK amount of interest and I don’t really want to trust my daily important money to fintech. I still use all the fintechs, but always keep a low balance in them and transfer in and out as needed.

There are just too many oddities, overall, that make them unusable to me. The trust factor, as you say, difficulties dealing with cash or cheques, worries about if I pay a significant sum in will I ever be able to get it out (Monzo’s forum chronicled how difficult it was to ever get their daily faster payments limits raised), support not being reliable enough to trust to get an immediate response in an emergency?

2 Likes

I read it, but I don’t know what to make of it.

I don’t think it expressly proves me wrong, but then again even if I wasn’t right then Monzo couldn’t prove it without releasing sensitive data (which I don’t and can’t expect them to do).

3 Likes

Thing is - and no disrespect to Simon - he has was in social/customer service. I don’t think he had any more insider info than Chris Skinner (and probably less understanding of KYC/AML rules/regs)

4 Likes

Not just that, but the perception of these fintech issues feels more widespread too.

I’ve got friends who’ve had Revolut pull things like this. Suspending access. Needing more info months or years since becoming a customer, or just shutting accounts down.

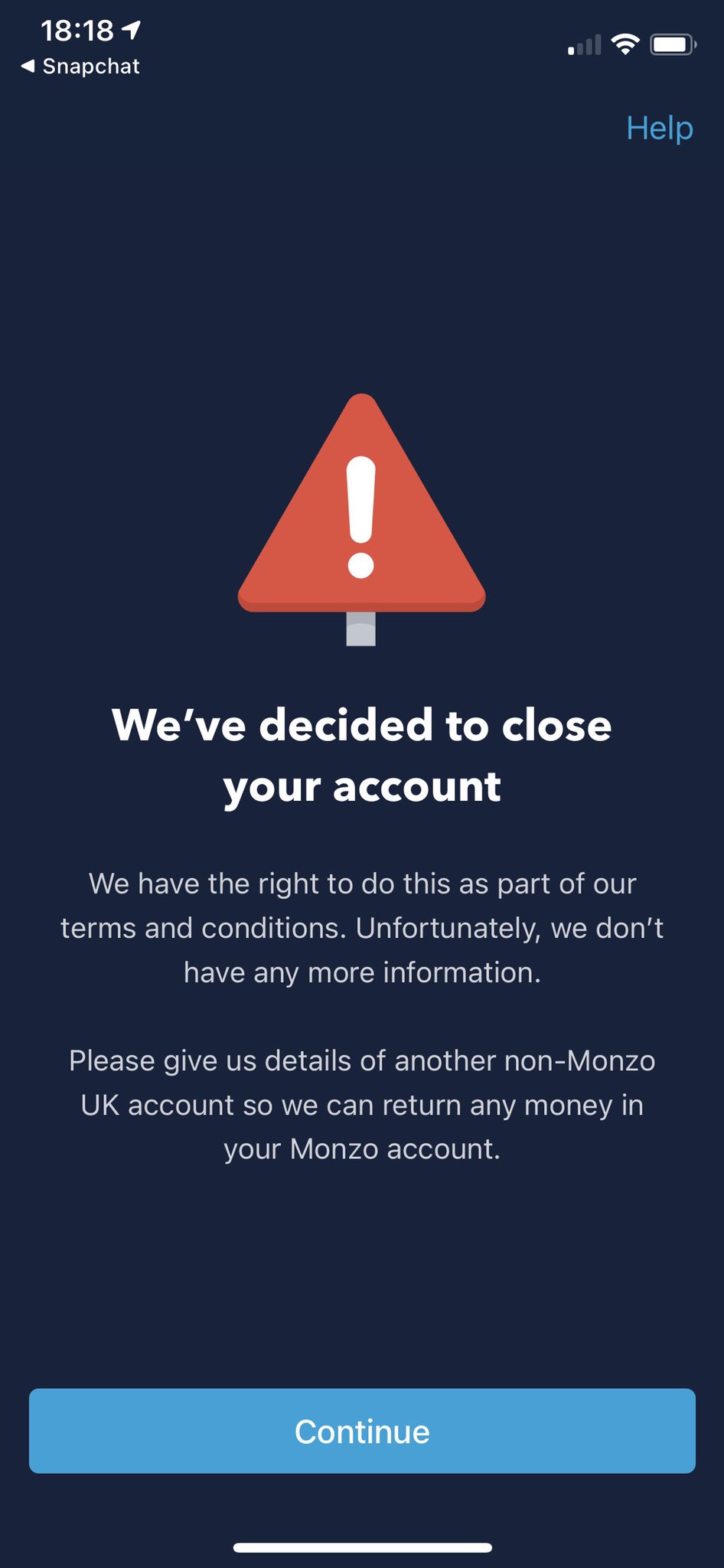

And I found out during the Santander issue, when the iMessage group chat lit up with my friend recommending Monzo or Starling to the Santander user, when his new colleague chimed in to say Monzo closed their account a few months ago after 3 years. They’re a junior graphic designer, working for my friend, fresh out of university. This is the screenshot they shared:

I did, I actually replied to him to probe for some information RE the email they sent me about a year after signing asking for my tax residency. As when I queried Atom for requesting that stuff earlier they said they needed to comply with regulations and continue offering me financial services, so even though he says their KYC wasn’t lacking, needing to retroactively collect additional information that is required to be compliant with regulations seems like a KYC oversight to me.

Agreed, and when he referenced a change in process in 2017, my first thought was “I signed up before that”, so straight away that was an admission that the process was not up to scratch at the time I signed up.

So should I expect my account to one day be queried/closed as a result?

1 Like