Agreed really, which is why I’m really quite surprised they are closing the branch at all!

Every other RBS (or NatWest) branch is just common or garden and can be absorbed into a neighbouring branch easily. Child & Co, Drummonds and Holt’s are the only special branches, so I always expected them to be virtually the last banks still standing after branch closures. They are also all currently on the RBS system. Hopefully Drummonds and Holt’s, at least, aren’t closing (they are not on the list currently, but for how much longer will any branches at all be around)?

Also, maybe they wouldn’t have to move sort codes necessarily if they leave the same weird setup as now. RBS and NatWest have been able to transact across the branch network for a while now, since changes to the IT system linked them together, and the Holt’s branch is technically both an RBS and a NatWest!

If that does happen, then maybe it points to them being dumped into RBS Premier since that is the system they are already on, although if the Child & Co branding is kept for existing clients then any of the other brands could provide the service, and just log in to the system necessary to do so. Coutts might do that?

Closing a branch and moving a sort code to notionally relate to another physical branch is a playbook they have run hundreds of times before and is relatively simple.

Sorting out how the more bespoke offerings of a branch are continued or wound down is a little more complex - I suspect the pandemic gave them an operational template for how the Child & Co service continues without a branch on Fleet Street to meet client in would work. The safe deposit operation would have been something of a headache, had they not opted to simply discontinue that service in which case they just need to give notice and ensure it is emptied.

Winding down a historic sort code, splitting out the ‘deserving’ customers from the ones who just wanted a fancy card… much much more faff than it’s worth. There’s a reason fancy cards are issued to all customers on that sort code (other than sub-prime/basic accounts), that reason doesn’t go away with the branch on fleet street being sold off.

The question really is when the Child & Co name goes, which fancy card do they start giving out instead. I certainly wouldn’t feel ‘downgraded’ if I ended up with an RBS Premier or Drummonds branded card.

All things being equal I would prefer the card I have now too. I don’t think Child & Co will be a thing in 10 years time however, not within NatWest Group anyway.

Could they not just convert 15-80-00 to a bog standard RBS sort code and then differentiate card etc. based upon the product held? I’m assuming that if you have a normal RBS account and then become eligible for, and upgrade to, an RBS premier account then you don’t then need to change your sort code?

That’s almost what they already do - the sort code is already on the RBS system like any other, just that customers at that branch have historically had different branding. In a way, it’s no different to First Direct being technically an HSBC account but with different branding. First Direct is not legally separate from HSBC, although some IT systems are different.

If you upgrade to RBS Premier as a normal customer at a normal branch, then your details don’t change. It’s just another product type - premier select instead of select account, for example.

They are already moving and reassigning the sort code, nominally, to a new location. They could, if they wanted, keep everything else the same. Or they could change things. We just don’t know until it happens. As others have said, it makes little sense to waste time and effort unpicking the custom setup so they may even leave everything as it is now, with all existing customers grandfathered in. That might make no sense from a branding perspective if they are closing the brand down, but if the brand is to continue for private clients then it could well be what happens.

Given they already provably can issue a different card based on factors other than your sort code, e.g. product held, one assumes there is a reason they have not limited it to Premier products only in all the years people have been getting these cards.

Either there are so many different products in there that it’s just simpler to give them all** fancy cards, or there was at least for a time a deliberate policy of allowing certain people to get standard RBS products but feel somewhat exclusive, perhaps the children of wealthy clients who as yet do not meet the requirements for an RBS Premier product but the bank still wanted to woo.

** in the days where there was a divide between Visa cards which required online authorisation and Visa cards that didn’t it seemed the ones who did require online authorisation (normally poorer credit individuals and children) would only ever get a standard RBS card but would receive a branded chequebook. In Natwest, this used to be differentiated by either a purple card (offline and online) or blue (online only). This in itself was a hangover from the ‘Servicecard xx0’ branded Maestro/Solo cards with the 3 digit number representing the level to which the cardholder’s cheques could be guaranteed… I remember being so excited about being moved from a grey Solo Cashcard to a dark blue Maestro Servicecard 250.

To add to that: Ulster Bank still used separate ServiceCard (debit card with offline transactions permitted) and DebitCard (debit card with online-authentication only permitted) branding on their Visa cards right up until the Mastercard switch.

Child & Co branded cards were also apparently only available to people with good enough credit history to qualify for an offline card (if your credit check would only allow an online card, it would be RBS branded, apparently). RBS Premier cards are also issued once you upgrade to a premier account, on any sort code. So card type can be changed easily at any time - I’d imagine it was always a deliberate policy, just like the Drummonds policy of limiting who got their card.

Apparently, based on old threads at MSE, there was some kind of drop-down box at account opening which allowed for selection of card type. Something was written into the system so that when an ordinary offline card was selected, it was replaced with a Child & Co card on that sort code only. Drummonds had a similar drop-down, except in that case the card type had to be specifically selected to be Drummonds Debit (if I remember correctly).

There was all quite a lot of discussion on it back around 2012 because, at the time, Lloyds’s planned divestment (known as “Project Verde”) to create TSB was also to be followed by RBS selling off a large chunk of business as part of the same EU competition commission ruling on state aid during the financial crisis. The RBS branches originally looked like they were going to be sold to Santander (rather than the later plan to create Williams & Glyn) and people discovered that, due to their special status in private banking, RBS was planning to retain Child & Co and Drummonds as the only RBS branches in England. So opening an account with them allowed people to avoid Santander and “stay with RBS”, plus enjoy the special branding too. That’s how the topic originally became prominent, although it’s possible (even probable) that personal customers could join the bank even before that.

I also see today on the MSE thread that somebody claims to have a Drummonds card, which I don’t have and have never seen.

It appears to be heavily based on the old “England and Wales” (to be Williams & Glyn) RBS design, and is really nothing special. I think I prefer the standard RBS Visa design that I’ve got.

However, they confirm that they are a personal customer and they are on the sort code 16-00-38, so the card is available to those customers. Although they say they had to request it at the branch, and some kind of criteria do seem to be applied. All very interesting.

And with Holts, you’ll only get one of their accounts if you’re serving or retired Armed Forces or worked for the Embassy or Diplomatic corp. I had a long chat with a Holts personal manager who despite being fully aware I was eligible for an account, put so many barriers up in terms of me having to present myself at a branch of NatWest or RBS or a personal appearance in Farnborough showing my eligibility documentation, it just didn’t seem worth the time or effort so I politely told him where to stick it.

As with Child & Co and Drummonds to an extent, the private brands are not really set up for automated checks and account opening.

So everything is a more manual process and requires more interaction, as you might expect from private banking in a way - where everything is tailored to the individual. Even when I opened my accounts online, I had to return signed papers by post.

Holt’s especially, because of it’s restricted eligibility, probably requires manual checks for every application and a personal introduction letter proving eligibility in most cases, and with you being retired they most likely wanted some less-easily-obtainable evidence. If you had attended the branch with documents, though, they probably would have posted it off and got it sorted. But I know that a special trip to a branch would have been annoying!

Now that I’ve discovered the Drummonds debit card exists I’m annoyed with myself for not pursuing it, I might have been able to get one! People from Drummonds and Child & Co did used to call me a while ago (when I had first opened the account) and they left messages, but I never bothered to call them back. I think I may have been allocated a personal banker across both brands if I had. Nobody has called since about 2019 now though. Oh well.

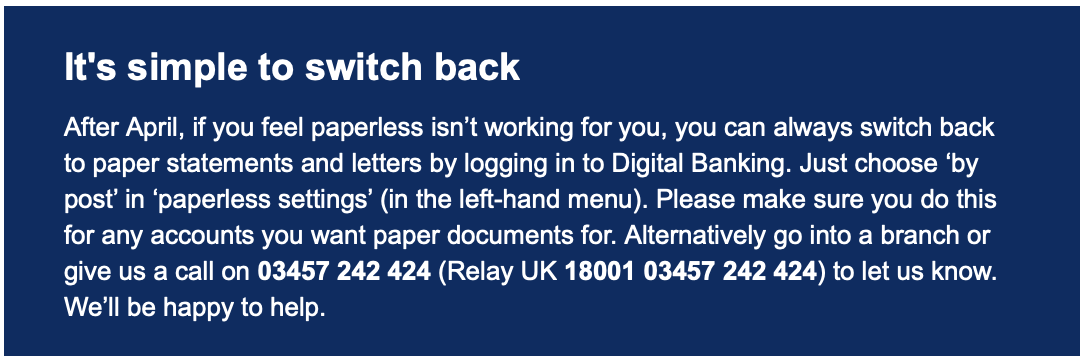

They’ve been switching people to default paperless statements for a while now (at RBS and NatWest).

You can still keep paper ones, but you must opt-out and I suppose they think most people will just accept defaults, so it saves paper compared to opt-in paperless.

Do bear in mind that all of the correspondence you receive will be written with RBS’s entire retail banking customer base in mind, there’s no conspiracy to get rid of the nice Child & Co stationary - or at least if there is it’s an entirely separate consideration to branch closure, pushing customers to online banking and paperless etc etc.