Hi all, a slightly niche query but I would like to tap into the knowledge often on show in this forum!

When considering investing in Triodos funds via a small SIPP transferred in from an old jobs scheme and some spare savings via a GIA. At the time I assumed the “No FSCS protection” disclaimer was the same as any investment in that the protection of your capital is not protected, whilst residual cash would be.

I have noticed some people emphasise the lack of FSCS protection due to the SICAV funds being Luxembourg denominated and outside of both protection schemes (UK & Dutch), but I think some are overestimating the protections FSCS provides to investments in the first place? (as they are not cash deposits)

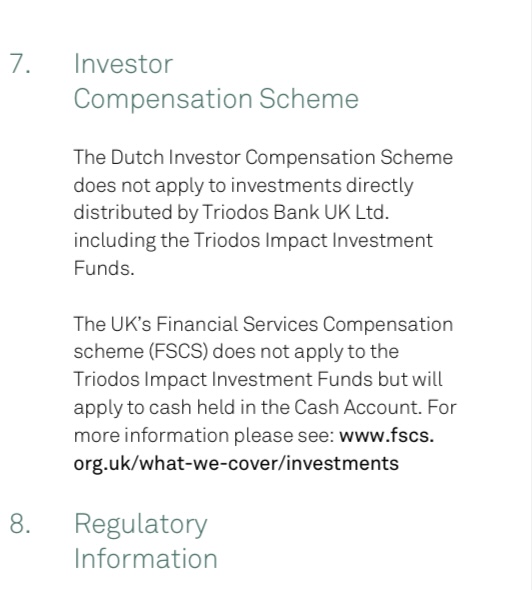

BUT from what I have read there does seem to be a distinction where FSCS protection can apply to investments of UK based funds, not for the value but for some instances like fraud, creditors dipping into assets, FOS judgements that cannot be paid for - am I right in thinking that it is this protection I miss out on by investing with Triodos? It would then be a case of considering this risk against their history in the market, AUM of over 5 billion et cetera? On the PRIIPS (x4) Triodos clearly state their Impact Investment Funds are UCITS compliant (would assist with any wind down) and that assets are held separately as per legal requirements so the proceeds could be returned in the event of a wind down. It just states that the value distributed is not guaranteed, which I understand applies generally. Am I right in then saying that I do not have FSCS as if the laws set by another regulator are not followed, the UK scheme is not willing to be on the hook (but the rules are still there all the same)?

I would greatly appreciate my logic being put to the test or any knowledge on this matter. It isn’t massive money involved, but it’s always good to be fully clued up on the risks you are taking and whether they are worthwhile. If my logic is right, I will probably persist.

Please note: I am not looking to discuss the general risks/costs/ethics of the investment (which are easier to fathom!), merely the investor protection.

My understanding of this is very limited, but I think you get FSCS protection (or equivalent across the EU) if you hold money in cash on an investment platform.

So if you used, for example, Hargreaves Lansdown, and had uninvested money within the platform but they collapsed, FSCS would cover that money.

Once “invested”, even in a “cash fund”, I am not sure you get any protection (as the money is now an investment, and not a simple deposit).

I think this works the same across the EU, so a Triodos deposit with Dutch Triodos would be protected under the Dutch deposit protection scheme up to the €100,000/£85,000 limit, just as in the UK, but if they did fail you would have to approach Dutch regulators to get your money.

If the money is not “invested” in Luxembourg, but physically held by as deposits by a licensed Luxembourg institution, then presumably the Luxembourgish system would provide the €100,000 cover.

So your question is:

Am I depositing with a covered entity?

What is covered by the guarantee, is the nature of the way my money is stored meaning I’m inside or outside the guarantee?

Usually, most of the time, investments are outside of the guarantee; hopefully that is clear from what I’ve explained.

I’m sure somebody else will be along soon to tell you if I’ve got anything wrong!

My understanding is that for Triodos the cash held in the linked cash account is treated the same as any other deposited funds, covered by Triodos UK Ltds license.

The investments are distributed by Triodos Uk but are domiciled in Luxembourg. So once you invest you are placing your money into a fund outside of the UK regulatory framework.

Please don’t see this as me saying I know better when I’m asking the question, I’m just hoping to sound out the community!

All funds do not have their capital protected by the FSCS but ones based in the UK (Vanguard Lifestrategy for instance) do advertise FSCS protection on the investment which I think based on my reading applies to things like: fraud (they never put your money into the assets advertised), maladministration (creditors have had to dip into clients assets to repay costs). So in the vanishingly unlikely event this happened to Vanguard or AJ Bell you would be covered.

I think Triodos will follow similar rules for segregation (it’s stated that by law all the assets are held with a depository separate to their assets) but as these are not UK rules the UK scheme won’t kick in to cover you if this did happen.

That said Triodos have 5.7 billion EUR under management so there would have to be a lot of assets missing and high costs for this to be an issue - if it did impact your holdings EU citizens would be bailed out but UK wouldn’t. I think I have it right?

Either way, it’s got to be an unlikely event, but it’s good to know what you’re opening yourself up to?

My understanding of the deposit protection scheme was that we were still covered, post-Brexit, equivalent to EU depositors, up to the €100,000 limit - just like the FSCS limit here.

This could be wrong.

I do know that with FSCS or the European Deposit Protection Insurance Scheme, you get the money back in the currency of the country it was deposited in (so, if a bank in Denmark fails and you have deposited, insured, with them in pounds or euros, you get an equivalent value of Danish Krone back from the scheme).

It’s a theory exercise, when Iceland couldn’t afford it’s FSCS equivalent the UK Scheme stepped in and covered depositors iirc.

Lithuania is potentially another Iceland in the making, but I think Luxembourg should be able to pretty easily cover everything it needs to. The rules are at an EU standard and they make a lot of money in financial services, which is contingent on them being able to cope with the level of financial services offered.

If the scheme was unable to cover depositors, I think they’d end up screwing over their ability to compete with countries like Germany, France and Britain immediately and for the foreseeable future.

I think Seb pretty much is right on everything though, you will get the funds back in EUR (not that it’s an issue? we’re still in SEPA and it’s easy enough to get a EUR account)

Thanks guys. What is odd is that the literature states that there is no FSCS protection and no Dutch protection, which I assume is to warn UK and Dutch investors as they may expect it to be so. However, there is no explicit reference of there being any Luxembourg based protection which is why I never considered there would be any! How would I go about checking this?

Also someone on another thread made the point that protection of this nature can be fairly moot and it’s best to consider the size of the fund/nature of how its run. Aka whether any fraud is at all likely. And in a worst case scenario, things like Investment Trusts and ETFs do not have FSCS for fraud.

My only thoughts here are that this seems to focus on bank deposits. This is standard FSCS style protection.

But there is a murky realm of FSCS protection regarding investments, which seems to cover maladministration etc in open ended funds which are UK based. But not things traded akin to companies like ITs and ETFs.

Now Triodos funds are certainly open ended, but where I have protection from any Luxembourg based scheme I have no idea! It’s not clear in the literature which only says Dutch and Uk don’t apply!

Either way, I think I have come to the conclusion that these protections are mostly focussed on fraudulent fund providers who haven’t got sufficient provisions for wind downs or are acting fraudulently - which I certainly don’t think Triodos will fall foul of. I guess I just wanted to investigate what exactly “no FSCS protection” means for an open ended fund!

I presume you’re looking at Triodos for ECG credentials?

If so, there are some FSCS options from other providers if that’s something you’d be open too.

Their funds are domiciled in Luxembourg and regulated by the Commission de Surveillance du Secteur Financier. As I understand it, I believe you’ll receive similar protections the FSCS provide, but capped at €20k as opposed to £85k.

Your cash deposits should be protected by the FGDL up to €100k though.

Hello there. This does make logical sense but what is odd is when you look at the terms and conditions it just mentions that Dutch/UK cover doesn’t apply, it doesn’t state that Luxembourg’s does?

Also, the cash in the account is still held as part of your Triodos UK account. It’s like another savings account really, so that definitely is covered by the FSCS. It’s just when it becomes invested that it becomes a little less clear.

Definitely worth asking them. There’s no clear information available to form a certain conclusion. but I do think this applies, at the very least either way:

“the SILL scheme does not apply toTriodos Investment Management regarding our SICAV-I funds, of which your K-R share class of funds are part of, because:

Triodos Investment Management is not to be considered a credit institution or an investment firm. Because in general Triodos Investment Management does not perform these activities directly towards individuals and therefore this SILL scheme would not apply in this situation.

Only in case Triodos Investment Management would perform individual fund management activities under MIFID II rules and regulations towards individuals the SILL scheme would apply.”

These are definitely relatively muddy waters and you can see why some opt for Royal London sustainable funds etc!

There are a myriad of ethical investment providers now with FSCS protection in the U.K. anyway thanks to the fintech revolution. Circa5000 (used to be called Tickr) off the top of my head. They’ve got ties to Octopus group. Complex corporate structure that group, not explored it properly in that context so can’t say if they actually own them.

I think their approach is interesting. Not a cheap fee structure for what it is, and you probably could just replicate it by going DIY, since their approach is entirely passive (there’s no active management). And whether it’s something that can actually deliver returns (particularly long term) is pretty untested. Worth looking at though if Triodos is a no go.

And of course the more generalist ones offer the option. I’m quite fond of Nutmeg’s ESG portfolio for instance. The fund picks are solid, largely made of UBS ETFs and they are at the forefront of ESG investing. Nutmeg have since been acquired by JP Morgan so naturally some folks will be justifiably averse.

Disappointing news nonetheless, but thanks for reporting back and letting us know.

No problem. I don’t think the material risk is really that high, but given a) I currently do my core banking with them b) the fact the protection isn’t there in a hell in a handcart scenario (e.g. market wide third party IT infrastructure issues or god knows what else) I have determined it probably makes it prudent to keep my ISA/Pension investments away from the same bank.

I have come across the Royal London Sustainable range - they are Multi-Index (unlike Triodos funds) UK Unit Trusts so there is no grey areas there. Perhaps not as dark green but they are actively managed and there is positive screening not just negative, the fund has achieved pretty good growth against the benchmarks and the fund manager was part of the Cooperative Banks investment arm before it was taken over. So perhaps as close as we’re going to get to a UK version.

I was considering the 40-85% (Sustainable World) for some pension funds and 20-60% (Sustainable Diversified) for some cash savings to account for the relative liquidity requirements on my side. In case you were interested (but may be old hat as these are well known funds) Sustainable Fund Range - Royal London

They aren’t available direct anymore, would need to use a platform. For passive investing L&G Future World’s seem a good option, but nothing multi-indexed here.

I will keep my Triodos investment account and treat it more like a play around should the feeling take me.