Is that with immediate effect or sometime in the future? I still see 1% in my app, 1.5% if I pay with mobile wallet.

This has kept me away from using the card

Is that with immediate effect or sometime in the future? I still see 1% in my app, 1.5% if I pay with mobile wallet.

This has kept me away from using the card

To be fair, with cashback capped at £10 a month, is this really such an issue? Does it actually really matter if it takes 5 days to get 20 pence back on a £20 purchase ![]()

It is, since I got options.

One time I had to chase customer support for cashback that had not tracked for over a month.

It just isn’t feasible for me if I can get the same thing from another provider

I get that, but it’s piddly amounts really. Not something I’d be bothered about personally.

They do not matter until they add up. The annual statements make it worthwhile.

I’ve fed that back a while ago actually, and it seems like poor wording on their part which I hope they fix.

It sounds odd to us who already have accounts, but to new users going through onboarding it makes a bit more sense. On the order your card screen you get to choose to order a virtual (encouraged and is the default) card, or a physical one, or both.

As I understand it, picking and spending on a virtual card will satisfy the requirements of the offer.

Yeah it does but the card order is a clear step. I didn’t want one tbh.

An oddity is it allows you to pick your card name so I just went for my surname for novelty.

Well, I’m gonna suck back massively on a post I made some time back stating that I wouldn’t touch Algbra with a barge pole.

Yup, with the aid of a referral from a generous individual tagged with a free £10 credit, I applied and was accepted within minutes. I received my card 3 days after application and I complied with the Ts&C’s and got my free tenner.

I’ve made several purchases using my very nice blue physical card with zero issues. I’ve so far had a whopping 20 pence back in cashback with more to come.

My initial impressions are that I like it. I like the App UI. I’ve had no issues funding the account either. So far, not a bad experience ![]()

I admire folks who keep their mind open to the point of eating their own words and changing their mind/opinion with humility. Good for you @Topsy2!

Well, if I believed everything I read on TP, I’d be a bit of an idiot ![]()

But you’re right, it’s about keeping an open mind. I’m not going to be stuffing large amounts of cash onto the card. I do actually really like the physical card, it’s better than the crap Starling push out ![]()

In which case, there’s no incentive to apply for this account.

I had similar concerns but stuck with the account and I’m really glad I did! Had some reasonable acceptance challenges with the HSBC Global Money account in Greece back in May and Algbra was a very handy Backup.

Absolutely no issues and support were very quick to answer any questions. It’s my only Fintech currently and so long as I can see will remain.

The account is fine. I genuinely send money over before a trip out or a purchase - buy it and send back any residual funds or cashback. How on earth they intend to monetise me as a customer I have no idea. It’s just a Revolut UI rip off with a generous cashback scheme but half the features imo.

Also they say they don’t use your money to invest in fossil fuels - it’s an e money account, how could they? Just like Revoluts statement of “we don’t use your funds for any risky business” lol

It’s less of a statement that they don’t, and more of a commitment that they never will. And that the partner banks they use for storing your money won’t either.

Which is where Starling and Monzo start losing some ethical points when this fact gets brought up. Although neither bank does, and they say as much, they don’t make the same commitment, and the lack thereof can just as easily be chalked up to the fact that they’re not really doing this with customer deposits yet.

It all depends on how much of an incentive you want doesn’t it? My incentive was a free 10 quid for 5 minutes effort applying ![]() The bonus was the person who referred me, also got a free tenner.

The bonus was the person who referred me, also got a free tenner.

This isn’t a serious account for me. It’s just an easy to use spending account that gives a bit of cashback. If I get a tenner a month in cashback, it’s better than the zero, nothing that I get on my Starling account. Oh, sorry, Starling paid me just 1 penny in interest on my current account for June whereas Chase paid me £1.23 on my current account.

Algbra isn’t costing me anything to run it and I’ll probably make the tenner a month cashback. There’s my incentive ![]()

@Topsy2 has it right - £10 bonus up front + frictionless onboarding and now…. 1.5% cashback. I’ll take some of that.

Between them, Chase & Algbra are nice to have in the pocket.

My comment was more in response to Topsy2’s attitude to “piddly amounts”

I didn’t bother with Algbra previously as I don’t spend much (tiny amounts using gpay) and already have chase and curve so wouldn’t benefit from the cashback.

With £10 bonus and 1.5% cashback I’ll definitely try it.

Anyone have an invite code?

Yeah dm me if you need one. They prefer to referral shared that way I think

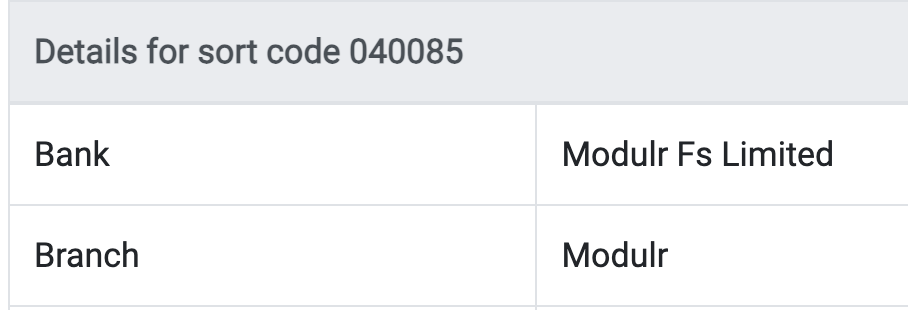

Who do they use? I can’t see this information readily available? Is it with Modulr?