Hi all

I’m looking for a way to earn a little cashback with a top-up or current account (but not credit card).

Haven’t really done it as such, only with Algbra, but the 1.5% with Google pay ends on 14th.

Open to suggestions ![]()

Hi all

I’m looking for a way to earn a little cashback with a top-up or current account (but not credit card).

Haven’t really done it as such, only with Algbra, but the 1.5% with Google pay ends on 14th.

Open to suggestions ![]()

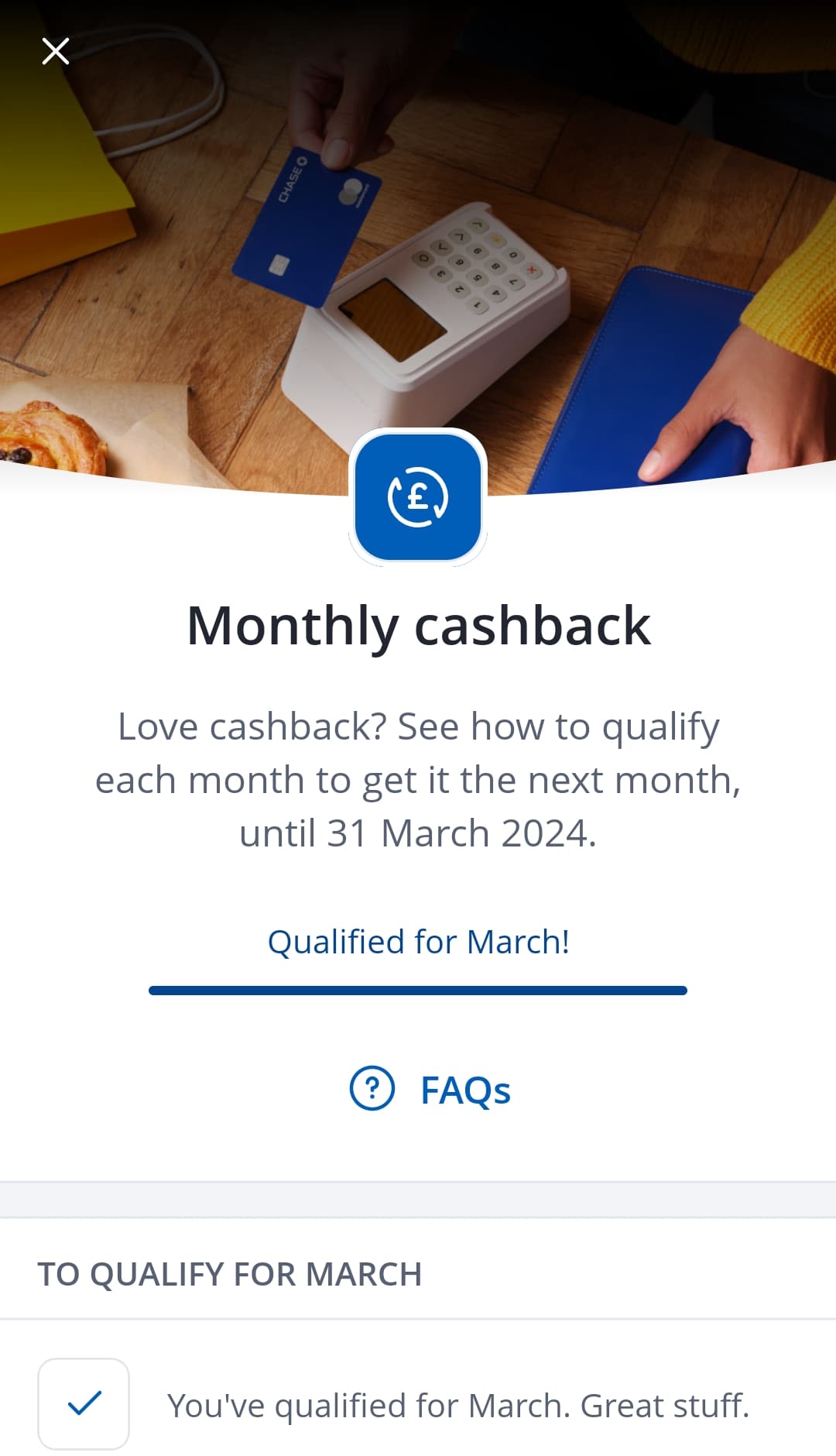

The obvious one is Chase, I have had this for a few months, spent enough for £15/month cashback at 1% on most spending (check the exceptions). My experience of customer service relating to a chargeback was also positive.

I’m interested in any other non-credit card suggestions.

Are they reverting to 1% after that?

If not, are they indicating what’ll replace it?

Yes. That’s the simplest solution at the moment (pity there’s a £15 limit).

Curve is another non-credit card though there’s a £9.99 fee (though the cashback is unlimited).

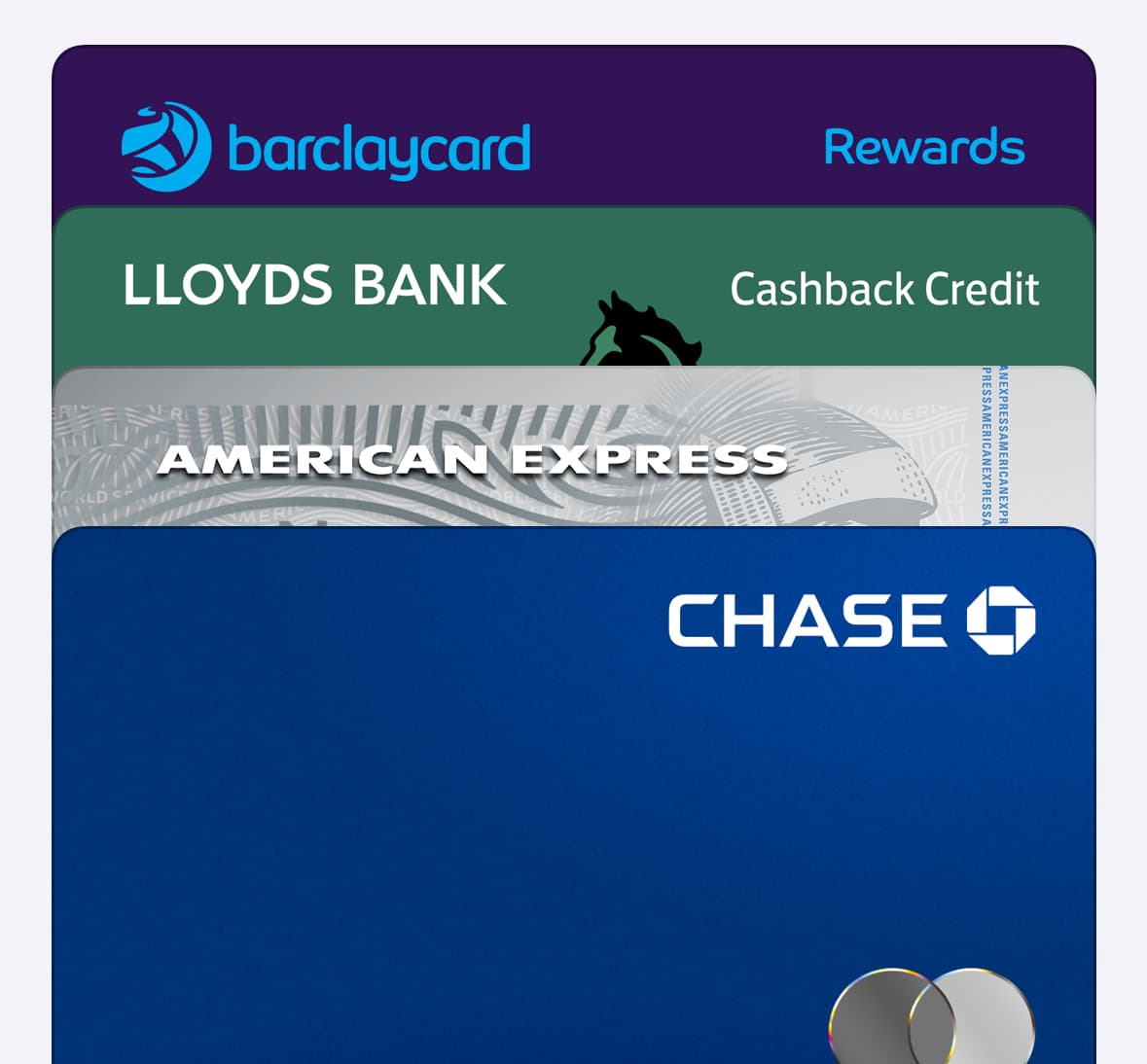

Chase + Barclaycard rewards is my day to day debit/credit combo.

There isn’t really anything else on the market that competes with these two IMO, unless you’d really benefit from Avios over cashback, then a case could be made for Amex. And there’s nothing else really on the bank side of equation that you don’t have to go jumping through onerous friction hoops for.

I also think the interest you’d earn by paying your bills through a Chase savings account (or paying them by debit card for cashback) will beat out what other banks will pay you for that unless you have very cheap bills.

Algbra’s has always been too slow, unreliable, and too much tacked on like an after thought that makes it more hassle than it’s worth relative to Chase.

I’m not really into the approaches being taken by the likes of Monzo.

It didn’t say in the app, just that it ends on 14th Feb (same in their terms

It was a customer acquisition tool and it’s ending. No indication it’ll be replaced with anything, or revert to 1%.

Worth noting the same is true for Chase. After 12 months, there’s nothing to suggest cashback will continue on for folks, unless they announce something between now and March. Or it pops back up as a new offer you can claim once it expires.

Blimey ![]() . What’s the attraction going to be now?

. What’s the attraction going to be now?

Good point. It was that which caused me to pull the plug on them.

Interesting that the website still offers wallet cashback with no apparent end-date (except in the t&c small print).

Edit: further scrutiny suggests the news/ blog is all rather old stuff.

Just the ethos and the ethical credentials I imagine. That was the USP from the outset prior to them offering cashback, and is what intrigued me and others like me. I was never there for the cashback personally and don’t much care for it, particularly with how bad the implementation was!

I think it also depends how Cubes evolves. The roadmap paves the way for features that could be implemented in a way that would out-Monzo Monzo IMO. So I’m particularly excited for those updates. Reminds me a fair bit of N26 Spaces.

Yup, I wouldn’t be surprised if it’s still on there after it ends. Though potential false advertising complaints might prompt a more prompt removal once the offer goes away (unless they extend it, which could still happen!).

It’s a relatively tiny team that hasn’t kept pace with their growth in customers, so they’re all too run off their feet just managing everything, let alone building the product out, to actually spend the the time needed on the more mundane things like that is my take away.

A very clear account. Thankyou.

That being said, I note my enquiries rather hi-jacked @Mathew’s OP.

Anything further in algbra will properly be aimed at its own thread.

*does a little cashback flex*

The debit card cashback options are pretty limited, though the credit card ones aren’t as good as they used to be either. Interchange fees are capped now, so most of the cashback offerings you see out there now are trying to hook you in so you make the company money some other way.

The Santander Edge credit card is worth a look, but costs £3/mo.

Halifax and Lloyds are basically the same thing, and Halifax offer a card equivalent to the Lloyds one above.

HSBC rewards credit card might also work for some people but it looks like too much hassle.

Mine is also going to die come April 2024.

A little sad, but I will be using my card in China through Alipay until they kill the cashback ![]() at least for smaller payments that don’t attract a fee !

at least for smaller payments that don’t attract a fee !

I am still plugging away with Plutus for now. Should be able to attain about £60 in cashback over the next few months as they offered me a few free months on the Premium plan to stop me leaving…

Halifax Reward - £5/month reward for at least £500 debit card spend:

Santander Edge/Edge Up:

Clubcard Pay Plus:

Far more lucrative sums are available with credit cards.

My personal ‘max value strategy’ is:

Notes:

Disagree strongly (as you know ![]() ) my picks would be:

) my picks would be:

Santander Edge Up Credit Card - 2% back in first year, 1% thereafter, £15 max per month cashback, £3/month fee. 0% FX too. Works out at 1.6% back on exactly £750/month spend in first year

Amex Nectar Credit Card - effectively 1% cashback (redeemable at Sainsbury’s, Argos or eBay). Chunky sign up bonus. £30 Annual fee after first year.

Barclaycard Avios Rewards - forget about air travel, which is a mugs idea of a good value redemption - it’s effectively 0.66% cashback when (automatically) converted to Nectar points and spent at Sainsbury’s, Argos or eBay

Natwest/RBS Reward Credit Card - 1% back at supermarkets and 0.25% elsewhere, £24 annual fee waived if you hold the matching Reward current account.

Has anyone mentioned Hyperjar? As this a debit card which OP stated as a requirement. Upto 1.5% cashback on “everyday spending” for new customers only, conditions apply etc.

Plus they have variable cashback on a selection of retailer gift cards, e.g. 3.5% back on Asda, 5% for Sainsbury’s, 1.5% for Amazon.

Interesting, hadn’t spotted they had an introductory cashback deal, looks decent:

Cashback Rates:

Exclusions:

Pro tip - Amazon gift cards can be purchased from self check outs at Asda and Sainsburys, using their respective gift cards ![]() this is my main way of funding my Amazon account.

this is my main way of funding my Amazon account.

Super Pro tip - buy Amazon gift cards at WH Smith using One4All contactless app, One4All gift card purchased through Complete Savings with 20% discount (max £100 per month)