Can’t fault you. I personally now find Starling so underwhelming, it’s boring. I’ve now moved my entire personal spend and salary over to Chase with just a token amount left in my Starling account which will remain open purely for the convenience of cheque imaging should I be desperate enough to accept such an out dated form of payment

Of course I’d really like Chase to offer joint accounts in the future and then me and the Wife would empty our Nationwide FlexPlus account over to Chase but we’d still happily pay the £13 a month for the insurance package with Nationwide.

If Chase do launch a credit card in the not too distant future and it doesn’t have much in the way of rewards, I’ll still apply for one. I’m generally only a 0 percent interest free spender, I have bags of discipline so I never pay a penny in interest. If Chase were to offer a 0 percent spending card even for six months, it would be worth it for me.

Heads up folks. I noticed when searching transactions were not showing up. I got in touch and this is the reply from the tech team

“Ron, your specialist, that you spoke with last March 18th at 12:50. With regards to issue you encountered when searching for a transaction on the app with case reference number xxxxxx. This is because there is a current limitation on search up to 200 transactions. We are working on surfacing this limitation and enhancing search to a wider range of transactions over the next couple of weeks. I do apologize for the inconvenience it has caused you.”

I’ll be taking my spend back to Starling if that’s the case. This plus they will now be reporting each sub account as a seperate bank account on credit reports is enough to put me off I think. I don’t know yet.

They are separate accounts though, so that kind of makes sense. As long as savings accounts won’t be reported I don’t really see why you’d need multiple, anyway.

Software jargon. Not sure why it wasn’t transcribed into plain English before it was passed back to the customer.

In essence, what we have here is a backend (server-side) limitation, with no sort of interface in the front end (client side- in the app) to handle it, which leaves the user confused.

Surfacing that limitation just means to add something to the App’s interface that removes that confusion. It’s usually for things like errors that don’t produce a meaningful error code, so you change it to produce something more meaningful: IE You surface what actually went wrong instead of hiding it from the client (or below the surface) so to speak. If that makes sense?

So what it sounds like is the short term addressing of the issue is to add something to the interface that explains why you don’t see more transactions, whilst longer term they work on engineering a solution that overcomes the limitation entirely.

Could be, indeed. But if so, much as I love ‘em to bits, repurposing “surfacing” as an alternative to “making something clearer”, is ghastly in the extreme.

@N26throwaway is right, perhaps I’m just accustomed to it working in the same world!

Sounds like support have reached out to product owner who’s given an answer which support have just repeated either without understanding what was meant or not understanding it’s not a term which universally makes sense.

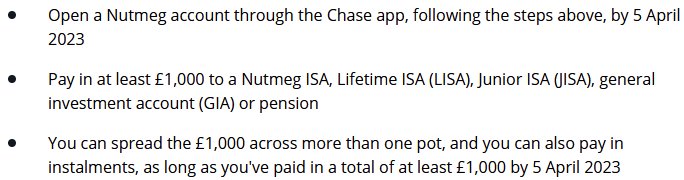

To double-check: Does the £1000 have to actually be invested in one of their portfolios (annoying) or just injected into one of their products (not annoying)?

In other words, could the thousand just be added to the GIA pot but not subsequently invested (applause)?

A Chase credit card would have to be a loss leader (like their current account) to be attractive.

I would imagine the reason why Starling haven’t yet launched a credit card is they’ve done the numbers on their customer base and it doesn’t add up.

With the interchange cap, no forex fees, bad debt, S75 costs plus cashback/points doesn’t make a profitable product. Drop too many of optional ones, no-one wants the product.

Carrying a balance is never good. Paying your statement balance is good for your pockets and your credit report. No one looks at a credit score. It’s a myth. It’s what’s in the report that matters the most

Nobody can prove this. It’s entirely plausible that there are lenders who do look favourably upon applicants with a history of carrying a balance, as this is often where the bulk of profits from their credit card operations come from.

There is plenty of anecdotal evidence of decent earners who clear their cards in full, every time, struggling to get the cards they want - Barclaycard Avios and Asda cards are the two that spring to mind. For issuers, there is no money to be made from straight forward interchange anymore.

Nutmeg are a robo investor. You have little control over your money once paid in. So yes, it’ll be invested according to the plan and risk settings you choose. A certain percentage will be sat as cash, but that’s not under your control.

Generally a lower risk setting = greater percentage in bonds and cash.

But once it’s in your pot, you have no control other than your ability to request a withdrawal or adjust your plan/risk settings.