Been using Curve card for a few months now, and find it quite convient, the only thing I don’t like is that transactions on the card used with curve don’t show the retailer, and just ‘Curve’. I guess there is no way around that, since it acts as a front.

Just wondering, if anyone is using Curve, and what everyone’s experience with it, or your reasons for not getting one? (i.e Apple Pay etc).

I used to use it a lot, due to it providing Pay and instant notifications, whereas my credit card (at that time) didn’t. Also, I used to use it when travelling. My current credit card provides instant notifications, I’m not yet travelling abroad a lot, and occasional issues with Curve transactions being rejected, and I’m not using it anywhere near as much as before.

I’m less bothered by transactions listing Crv* before the retailer name, and I certainly don’t only get Curve…

I used to use them a lot, simply because I thought it was a cool concept (and because they offered cashback back in the day - don’t know if they still do). Then they became unreliable and I had to chase up customer service repeatedly to fix issues (often only resolved after weeks long delays and calling them out on Twitter).

Got fed up and closed my account. Asked them to delete all of my data (except those pieces required for regulatory purposes), which they didn’t do: To this day - despite repeated complaints to both them and the ICO - they are constantly spamming me with marketing emails.

So, my opinion of Curve is, erm, pretty negative …

They shut my account way back, when they decided they were going to start charging for HMRC payments.

I’d used them to put my tax on a credit card, which was pretty lucrative for me at the time.

They claimed I was “cash recycling”. When I asked exactly why they thought that, no explanation was given and they closed my account. Or tried to, as I can still actually log in years later…

Really, I think I was just an expensive customer and they were culling accounts they no longer wanted.

The whole Amex debacle didn’t sit right with me either. I felt curve were somewhat economical with the truth.

It’s a shame the company presents so badly, when the product is/was interesting.

I still use Curve, so that I can use my Barclaycard through Google Pay, and my Chase card, again through Google Pay, to avoid the app authorisation issue in local rail app.

Outside of those specific uses, their other features don’t interest me.

I found it unreliable and as Google Pay matured, it’s USP diminished for me too. Also, usage nullified S75 and was never confident of their CS should I ever need to chargeback something.

Less importantly, i found their business model strange - they could just about break even with debit card recharging, every credit card recharge will operate at a loss.

I used to love curve and had curve metal. Until CS never improved. I want to say it was never good in the first place. Now there’s better limits on Apple Pay and most credit cards are supporting mobile wallet I see no purpose.

I was lucky enough to get my hands on a Curve Tumi Wallet

I think the “etc” is worth highlighting: Samsung Pay, Fitbit Pay, Gamin Pay, SwatchPay. This makes it useful as a pay conduit for users of a wide range of smartwatches, which are often not directly supported by banks.

Another thing that hasn’t been highlighted is it provides a way to use rewards credit cards abroad without currency conversion fees usually associated with rewards cards.

So although I don’t use Curve all the time, I do find it a useful thing to have.

Comes with a big asterisk though that you give up pretty much all rights that you’d normally get, having to place your trust in Curve instead of your bank

Comes with another big asterisk of fair use + maybe not really the proper exchange rate over the weekend + if your card actually has no charge to begin with, it doesn’t support pass-through currency charging; so you may a) bite into your allowance of “free FX” or b) get charged for a transaction you wouldn’t have

Fair enough, just for me the service has become redundant at this point. I haven’t had enough good interaction with their CS to trust it more than my bank’s

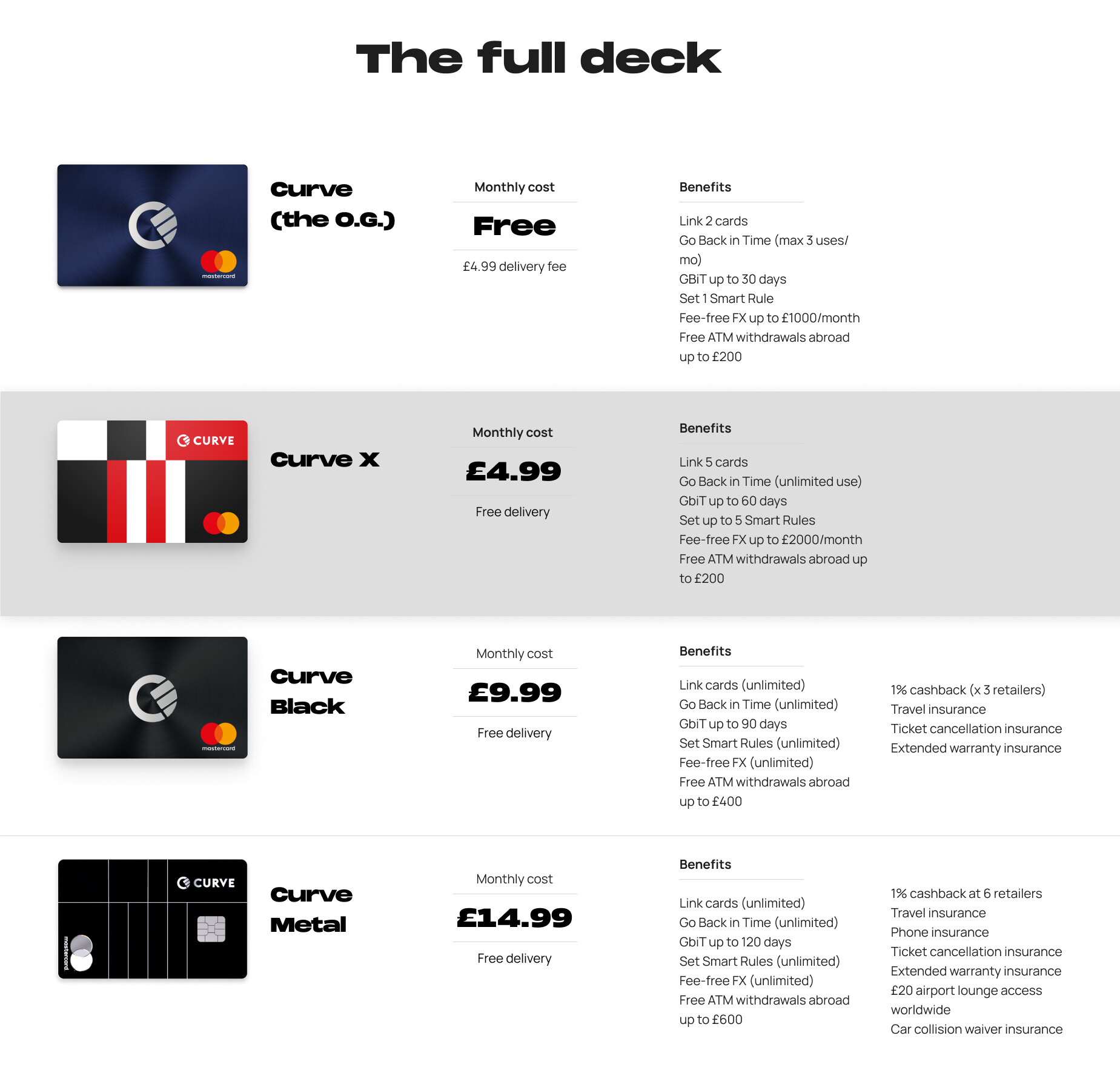

Ha, that’s quite misleading ! It should say “We are completely trashing all tiers below Black in a desperate and doomed attempt to stay afloat” but I guess “Introducing Curve X” is a little bit, er, snappier