‘ Good evening, thank you very much for contacting Secure messaging Support. I hope you are doing well today. I will be happy to help you today.

You can give us any bank details to set up a direct debit, if you pay in full no interest will be charged, please do not pay it manually as the direct debit will still be taken. You can choose to cancel teh DD anytime you want.’

It could be because I’m paying the minimum amount by DD at the moment. I’m using it as an interest-free loan for a single large purchase and I’m paying some myself in addition to the minimum.

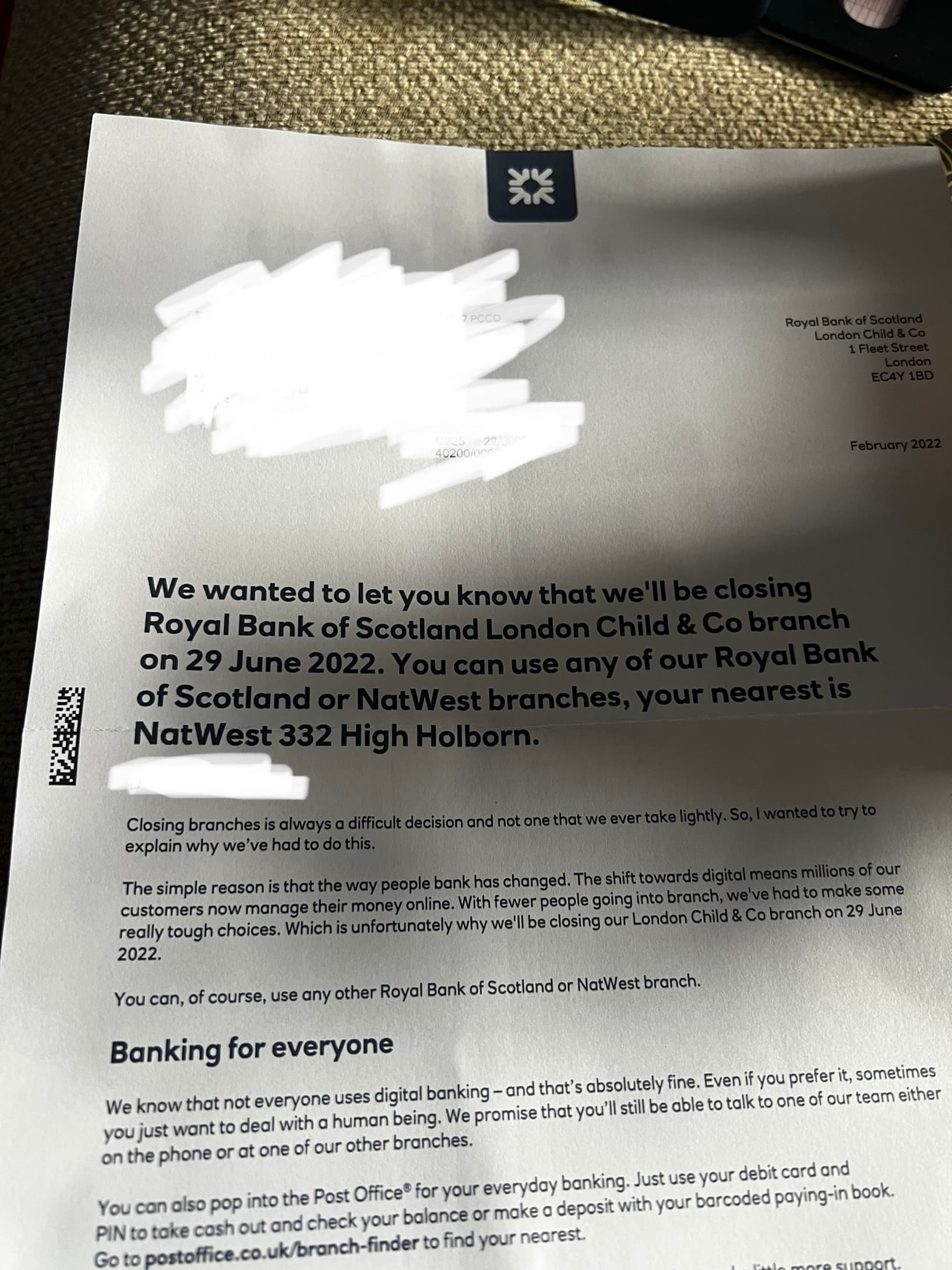

Has anyone closed an RBS or NatWest account before via a switch? When you did so did it leave other accounts - such as a credit card - open and accessible in the app?

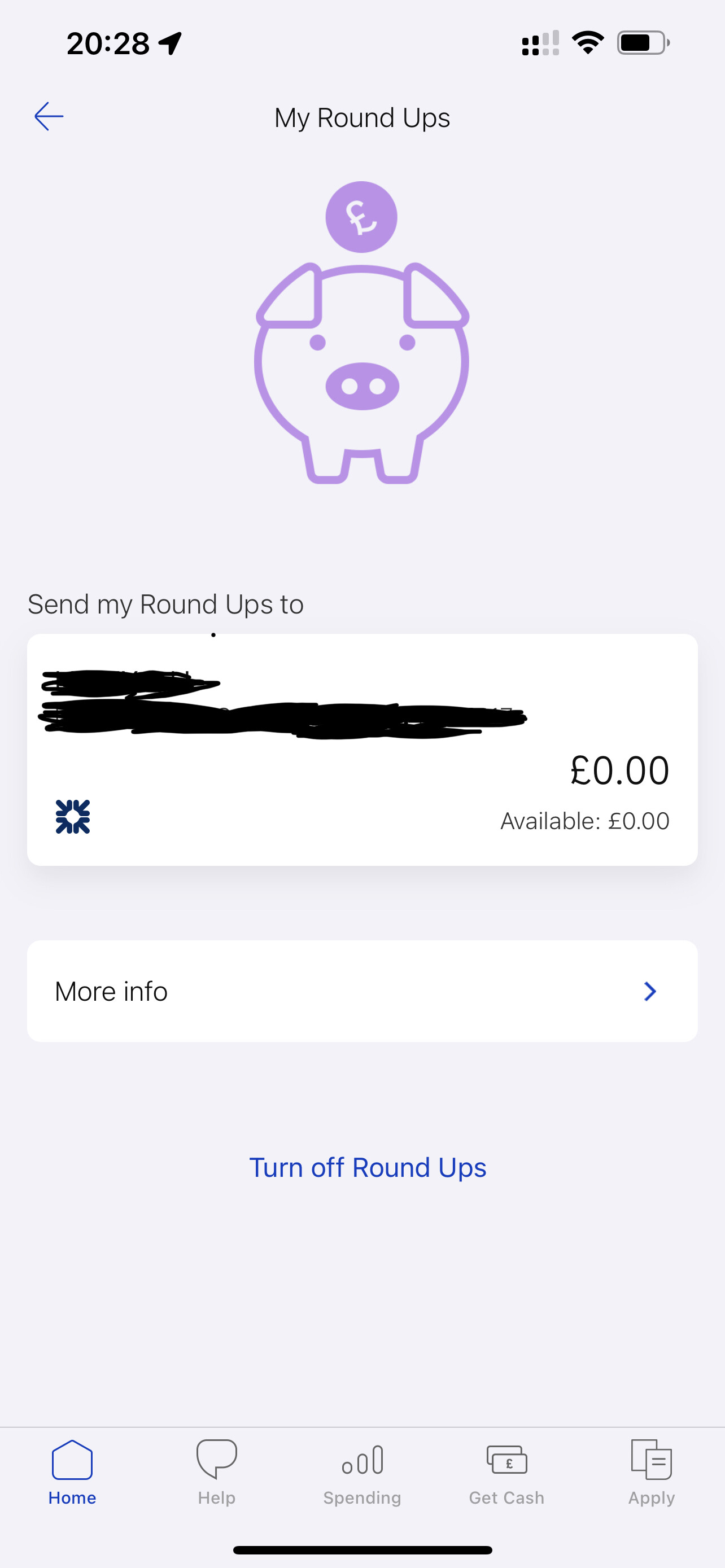

Having looked at the in-app FAQs on this feature, there were a couple of points I found interesting:

The round-up happens once at the end of the day. So it calculates your total daily spend and rounds-up on the total, rather than per transaction (for example: spending £0.73, £1.52 and £11.23 would result in a single round-up of 52p rather than many separate round-ups).

You can turn on round-ups and save into your Digital Regular Saver (if you have one) above and beyond the maximum contribution via regular standing order. So this could be a good way to make extra savings at a decent interest rate - the interest rate on that account is currently 3.04% AER.

Yes, if you don’t want a messy feed, but perhaps not if you want to maximise your savings (although the wisdom of using round-ups as a sole “passive savings” strategy is somewhat flawed, it’s better to put aside lump sums on a monthly or weekly basis and potentially use round-ups as a “top-up” on that).

Where it does fall down slightly is that the round-up happens once all the card transactions have been cleared, so effectively a few working days later. I see why that is (as then you have a final “daily spend” figure to go off) but it does make it a bit clunky. I think it would be better if it happened overnight every day using the values of your pending transactions instead, and never mind if the round-up then happened to be slightly off when the final total came in - after all, it could only ever really be out by about a pound.

It’s an easy way to passively save without really noticing or taking much of a hit financially.

It keeps my bank balance nice and rounded.

#2 being the most important to me. I think I’d like an approach that worked retroactively. Set aside an amount based on the pending charge, then finalise it once it’s cleared. Where roundups always fall short for me are for things like grocery shopping, where the transaction almost always settles at a different amount than the pending charge unless you shop with Ocado. So it undermines one of the aspects of round ups for me.

Another is in the instance of holds and cancelled transactions. These should never settle and the funds eventually get returned. But for banks who do roundups, you don’t get that part back, it stays wherever your roundup goes.

. Wonder if they’ll keep the card logo?

. Wonder if they’ll keep the card logo?