not really, the cards are now all the same colour aren’t they? the only distinction is the top right (useless for people who can’t read and have two accounts, or people with poor eyesight that either can’t be corrected by glasses (or don’t have any)) as to the card type

also worth mentioning that it loses all the charm of the old branding, which looked very trustworthy and professional (pewter grey branch in swindon was great)

only a twonk would decide to change banks over a branding change, much more important moral stances to take

i am salty about it too, imo you’re a member or you’re not. but i accept that we can’t change it / it is what it is

they REALLY stress this, when you do one of their apprenticeship tracks

I don’t really think Nationwide participates in any lending that’s particularly scary balance sheet wise, seeing as the majority of their lending is going to be credit card / mortgages (second being secured)

this is a legitimate concern, for a year or two more yet. i suspect afterwards wifi people will probably start offering satellite services for areas uneconomical for connection to a fibre network (using the satellite for backhaul)

understandable, maybe I can get Premier with HSBC Mainland China and port the status over to Britain; although I’m assuming that the capital requirements are easier there

edit: it’s 500,000RMB (56k-ish in pounds) balance, aggregate across your accounts (or still 500,000 for HSBC premier family)

Well, yes, sorry for veering off topic. But to answer you, when I bought the insurance (some months ago before summer) I never considered that it might be cheaper to get it via a bank account. I’ve never had a packaged account, and never done a switch before seeing the nationwide offer and just deciding to go for it. When deciding which type of account to open, I immediately discounted flexplus as I assumed all accounts with monthly fees were poor value. It’s really only earlier today (technically yesterday now) that I read the messages on this thread and realised flexplus could actually save me money…

Monzo in particular are reading their forums so feedback can potentially lead to positive changes. I “moaned” about their new app design while it was in Labs but then switched to another bank when it was formally rolled out and I still disliked it.

Equally, we’re all adults and banks are institutions that make mistakes. Sometimes the right thing to do is engage in conversation and try to remedy the situation. You can be annoyed by something without it ruining the relationship completely.

There’s a time and a place to moan, a time and a place to persue complaints, and a time and a place to take your custom elsewhere

It’s you that doesn’t realise that significance of difference of being a member v a simple customer.

To be fair, they do seem to training their staff to avoid avoid using the term member.

I was last called a member prior to them closing three local branches and relocating a fourth.

I couldn’t agree more because quite simply as previously stated, I don’t care. I’ve never even voted in their AGM since I became a customer all those years ago. I might be miffed I didn’t get the free hundred quid they’ve been chucking about, but I guess I’m mostly to blame for it

God I wish, then I’d get away with no wallet anywhere. But, I have a feeling it would also encourage smaller merchants who want to avoid taking card payments to just install an ATM instead…

there’s already a few that lost my business by pretending the card machine wasn’t working when it was imagine if they dropped support entirely in favour of an ATM in-store that they could skim 50p on in the process

I think I’d like it so much if they kept the blue.

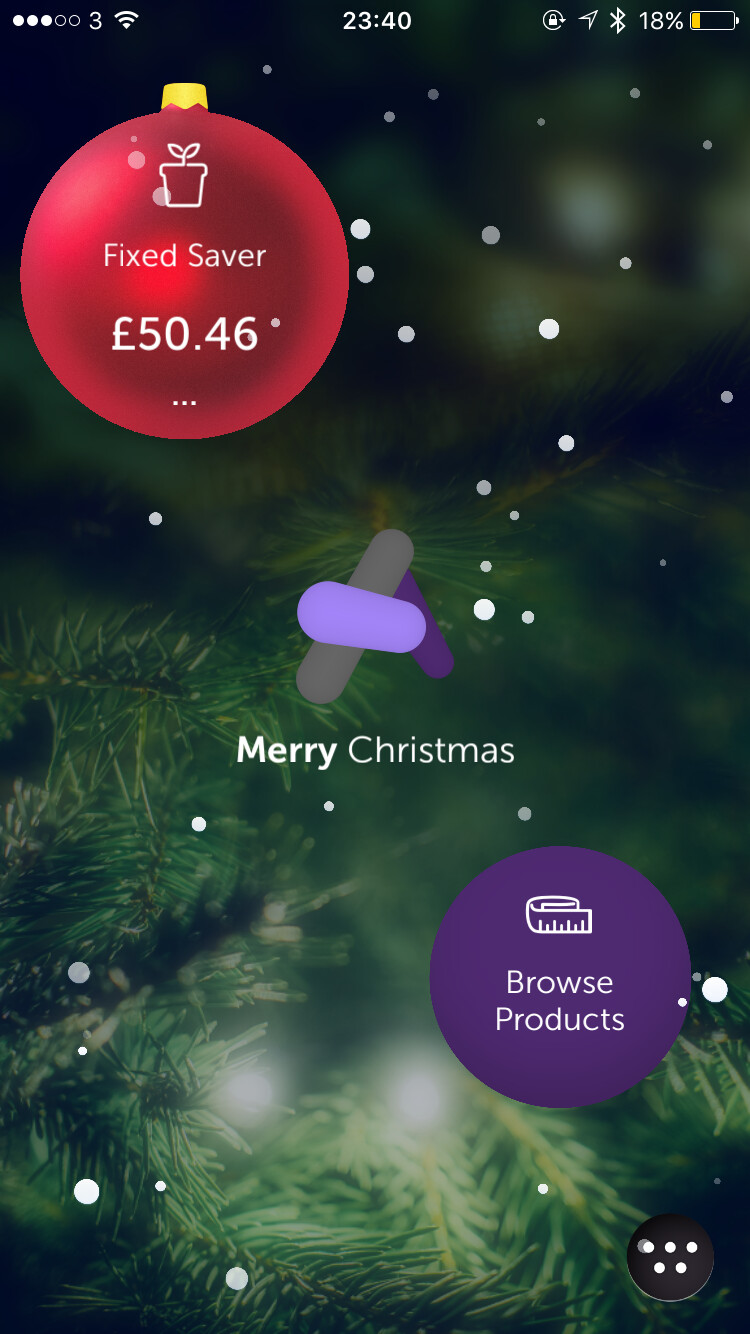

It reminds me a bit of my old Atom Bank logo/palette (anyone remember when Atom gave everyone their own custom logo?). It’s a bit too much and too many shades of purple. It’s begging for subtle complimentary accent colour like a nice shade of grey or a blue.