I used to have curve, I actually got rid of it twice.

The handling of the Amex situation was dire and at every opportunity they seemed to be wipe out all their USP’s (something that the moderators did not appreciate me saying on the community)

Is anyone here actively using Curve and has it got any better (without having to pay for the premium product)

Apologies for the title but I had to make it more than 15 characters

I just tried to create a new Curve account for the £10 referral via TopCashback, only to be told that the account I closed in 2020 is still there, with my mobile number attached to it, so I cannot create a new account, but can re-open my old one

Only need the darn card because BarclaycardPay will not work on my latest phone, so need a shell for the contactless (non-carrying card) feature.

As my Tesco CC is also not supported by GooglePay, I may add that one as well.

Don’t know what it looks like yet, as cannot get back into it yet

When I closed my account all they did was put ## at the beginning and end of the email address. It basically meant that I could still log into the account and prove to them it wasn’t closed.

I don’t think they have the ability to close accounts I think all they do is put random numbers in the telephone number and something random in the email field

It did get more reliable, and I used it especially for instant notifications where the underlying card didn’t support them. Plus it was better than many cards when travelling with better exchange rates / less fees.

With less travelling and more cards offering instant notifications / ability to see pending transactions in the app, it’s had less usage of late.

I still like it for not having any number details on the front though, which I wish more traditional backs would adopt.

Yes, and, whilst technically online transactions, have the location of London, which caused one of my CCs to invoke their fraud triggers whilst I was travelling and had used it for both local and Curve transactions.

From experience can you make a card payment with a virtual curve card after signing up, do you think that would trigger the eligibility for the top cash back offer?

I have an account but don’t activity use it. Only reason I keep the account is it can act as a bridge between Garmin Pay and Monzo. But I don’t need that very often.

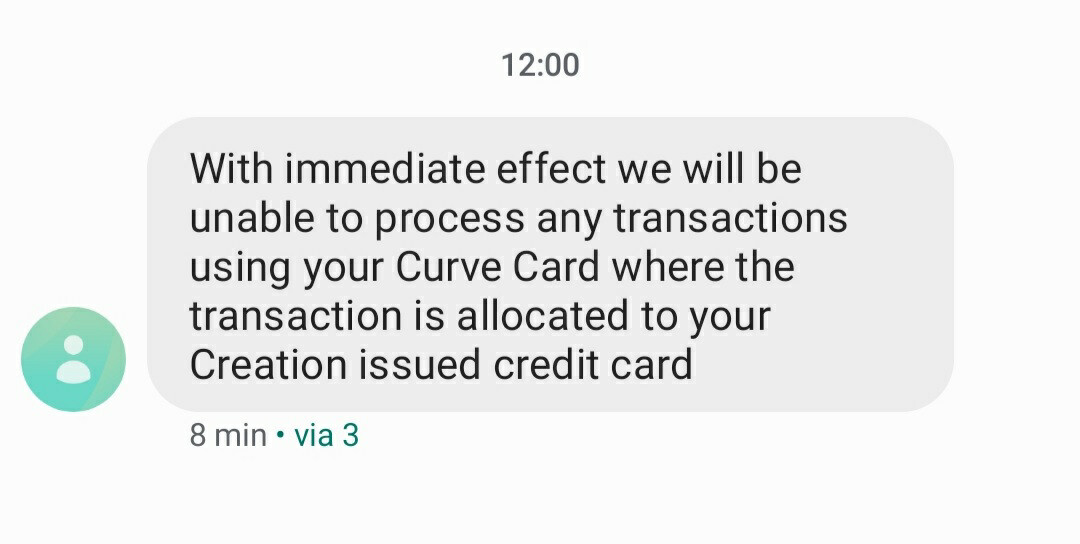

Regarding Amex. Not sure what else they could have done. I didn’t follow it closely but what I recall is Amex blocked Curve.

I think part of curves issue was the fact that they tried to blame it on AMEX when it was obvious to everyone on the community that they were at fault for making a series of assumptions and then not actually trying to work with AMEX.

IIRC they did this big song and dance about working with AMEX but then turned around afterwards and said we were working within the rules and AMEX have no choice (Which clearly wasn’t the case)

Curve forgot that they were using AmEx network for processing and can end the relationship at any time for any reason, as is stated within every merchant contract on planet earth

I don’t believe for one moment that Curve forgot about anything. I understand AmEx had two particular axes to grind with the whole concept:

If a customer has a problem with a transaction charged to their American Express account via Curve it makes for a difficult customer experience. AmEx pride themselves on customer services and putting things right when things go wrong. However they have no responsibility for a problem where a Curve card is used to make the payment.

And more importantly it undermines (commercially) the need for need for American Express card processing network. Which also risks lowering acceptance.

Had Curve actively engaged with American Express early on, these things would have been quite clear from the start.

They could have probably gotten rid of the #1 & #2 reason if they made it A) for Curve business customers only and B) a subscription you’d add on for access to it and C) AmEx handle the CS for it

That way AmEx still get their higher fees, provide good customer service and it’s not so easily accessible; it would only be worth it for high spenders at lower types of outlets, not all the retail AmEx clients that are going to their local takeout (i.e. the ones who wouldn’t want to spend on fees)

In another nice piece of news, both of our card machines at work now accept AmEx, they did it without asking too (Lloyd’s Machine)