I love Chase but I hate Chase and it’s so close to falling out of use as main spending card that it’s already happened and I’m in denial.

The app is slow and archaic, a bigger chore to use than for many legacy banks. There’s always some problem causing some outage or some delay to transfers. My local Sainsbury’s nopes at the sight of it more often than not. In fact I’ve never had a card decline so much for no reason.

The 1% cashback will never get old, but it’s really the only reward left worth a damn. The 1.5% instant access pots are long since outdated and the 5% round up interest is a bit of a red herring, really.

But really, beyond all that, the lack of Open Banking is making it just plain fall out of favour/use in comparison. Part of the issue is I have way too many accounts, admittedly, but being able to see them all in one place, budget all together and easily move money around is invaluable.

I’m definitely not Monzo’s demographic, but it always finds a way to end up front and center in my accounts - laziness most likely being the chief cause.

@stevenje not very nice mate, if you disagree with my personal experiences feel free to post why

I think you’ve perfectly captured my general sentiment with both Chase and Monzo beautifully here too.

I’m exactly the same way. I really like Chase, and when it was without issues and leading the market in areas, it was a wonderful experience. The magic is mostly gone though, and the honeymoon period is over.

I still really like the app and the overall package though. But I always really like Monzo for the same reasons. They’re vying for the same roll in my financial life, and I’d love to use both, but I don’t need both, and right now Monzo is winning for me.

Chase carried my group through a holiday last year and it made a great benefit to the trip in a way no other bank has for spending abroad. It was just a joy, and I miss that feeling.

And yet despite what has been said above, this morning, I had an absolutely instantaneous fund transfer from Starling to Chase. It seems that since I was finally able to confirm my account in my Starling App, things have improved.

I can’t deny, I’m a huge Chase fan now. I use the account every day for my personal spending. It works well with Tesco Pay+ the savings element is keeping me happy. It’s way ahead of FD in my opinion and I like the App better than Nationwide’s clunky offering. It’s all opinion though and as I’ve stated many times, opinions are like butt holes, everybody’s got one

I can’t be too critical of Chase - I’ve made £29.41 in cashback so far - but it’s finding itself falling out of favour/use and being replaced by more functional options.

It’s a bit easier for me to ignore Chase with the 1.5% interest rate no longer being competitive - but I do wonder if this is maybe just the way it was always going to go for me. The financial benefits of Chase ultimately falling behind the ease of use and reliability of Monzo/Starling.

I could probably agree the RBS app is better now, compared to Chase (ignoring the menu upon menu). Starling and Monzo last I checked have fallen a bit behind. Especially with the “payments from goals” thing Starling has done. It’s gross.

Big up the rest for having web applications though(assuming Monzo does), even if Starling did take ages to bring it forward.

Odd, maybe we buy things at different times: never had an issue with it (personally).

Probably why they’ve extended it until February. My problem is with places like Chase etc, is the second the competition outdoes them, you see that very quickly it was a loss leader, rather than them coming to flex their muscles with the “Reward Banking”.

? I have like £200 in it, with several hundred put on my credit card instead of Chase; I’d say it’s pretty good.

Should also mention the best feature of Chase: multiple account numbers.

I feel like comparing anything to Nationwide is like seeing the lady from the Scary Movie franchise, the scene looks like it’s going to be rather lewd, then suddenly there’s a chastity belt. Nationwide feels like a bank until you need to do anything: then you encounter the chastity belt. Extremely annoying to use.

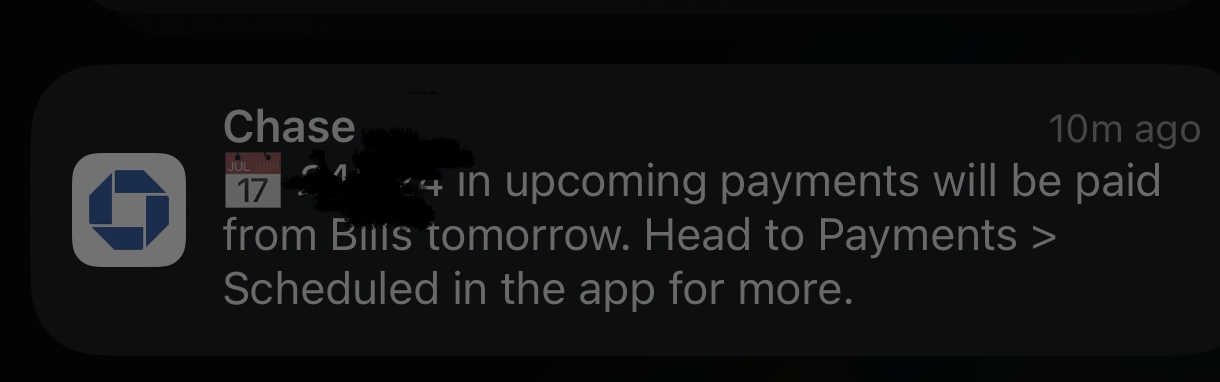

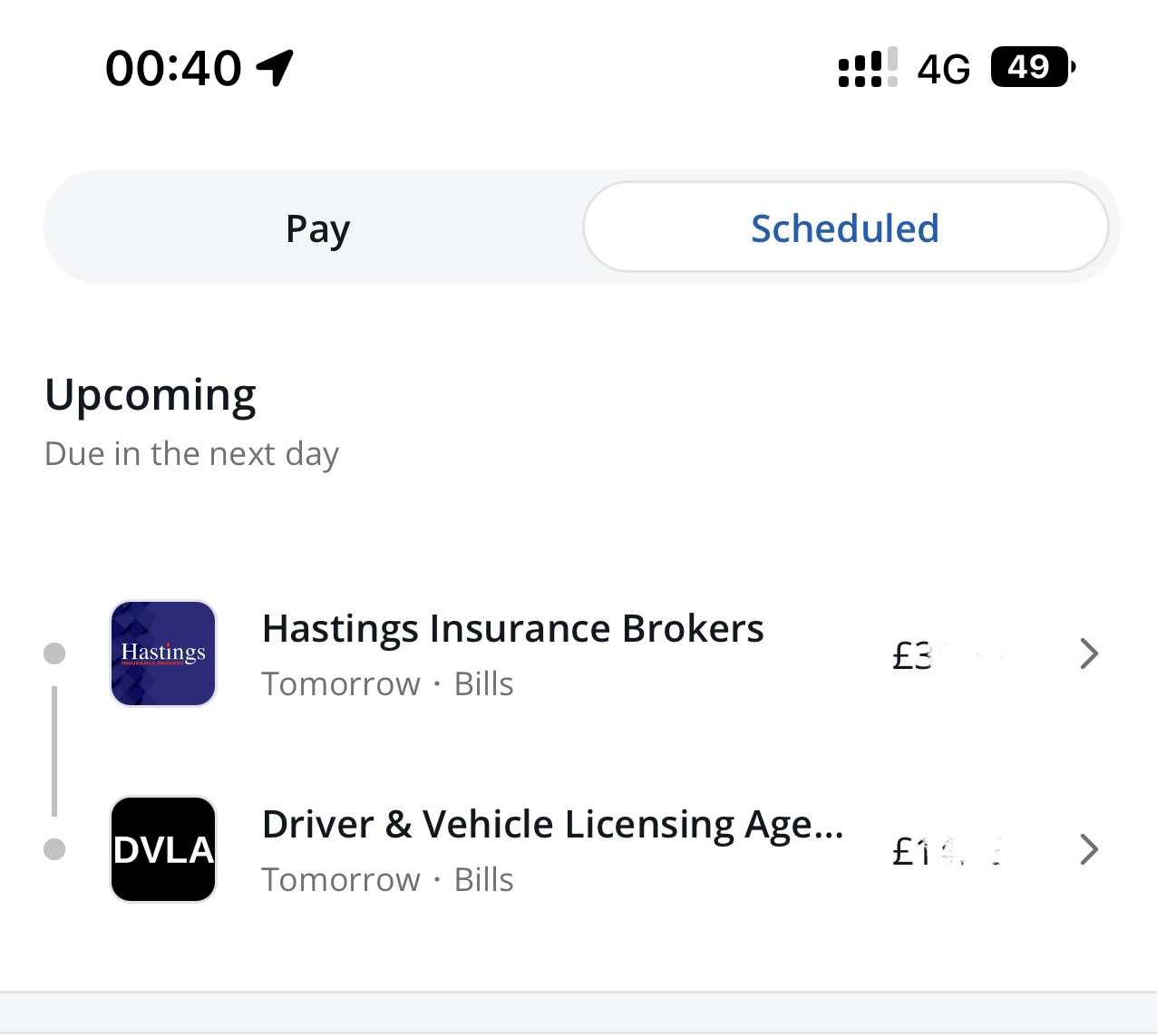

Chase have indeed added a new upcoming payments section and Direct Debits that are due to leave my account tomorrow are shown and I’ve received a notification to advise.

This is much improved over the previous iteration and I’ll soon be moving all my DD’s to Chase and will be using it as my primary account. I also feel that payments into my account have also speeded up.

For me it’s not about cash back or any other offers, it’s about the brand and the app is much nicer than Starling (I’ve now closed this account) and although I’ve been with Monzo from the start I much prefer Chase and I do believe in the coming months and years they’ll be much more on offer - like transferring pensions and credit cards - maybe we’ll get a packaged account too - who knows. I do believe Chase are listening and they are making improvements- not as fast as some would like but at least it’s happening and I’m glad they’re sticking around.

Well I don’t know about anyone else here, but I’ve so far earned well over a hundred quid in combined cashback and savings interest from Chase. In contrast, Starling have paid me less than a quid so far in interest (this year)

I do of course hope Chase will expand much further here in the UK in respect of the current account offering. I too would like to see a joint account, a credit card etc.

If Chase show themselves to be committed to the UK banking scene for the long term, I’ll happily move my salary and pension from Starling over to Chase.

I use my Chase debit card only where Amex isn’t accepted, so only get about a fiver in cash-back per month.

Where Chase really shines is using a saver account as a current account - my DDs and SOs come out of it. So I get 1.5% interest on most of my “current account” money. Elsewhere I’d get zero or very close to zero interest if I used a proper current account.

I don’t keep much in the Chase current account as (1) I don’t earn interest on that, and (2) it isolates your card from your main balance. As I say, my spends generally go on Amex.

I’m in the same boat, and with the slow climb in interest elsewhere the savings account is slowly losing its appeal to me as I’ve got a system going whereby my money is generally where it needs to be aside from a small amount I keep in current so the saving would be negligable.

Whilst appreciating that there are savings accounts out there paying higher interest than Chase, unless you’re prepared to tie your money up for a considerable period of time in order to get a decent(ish) return, I’d rather at this point, just stick what I’ve got in my Chase savings account.

I want easy immediate access to my savings, I don’t want to have to give any notice, so I’m prepared to earn a bit less. I have of course looked at the likes of Zopa and I’ve even looked at Barclays 5% odd on up to £5k,but I honestly couldn’t be arsed to open up a Barclays Bue Rewards account just for that.

Unless other savings providers start knocking out immediate easy access savings accounts with rates of at least 3% no strings attached, I’ll just keep my money with Chase for the time being.

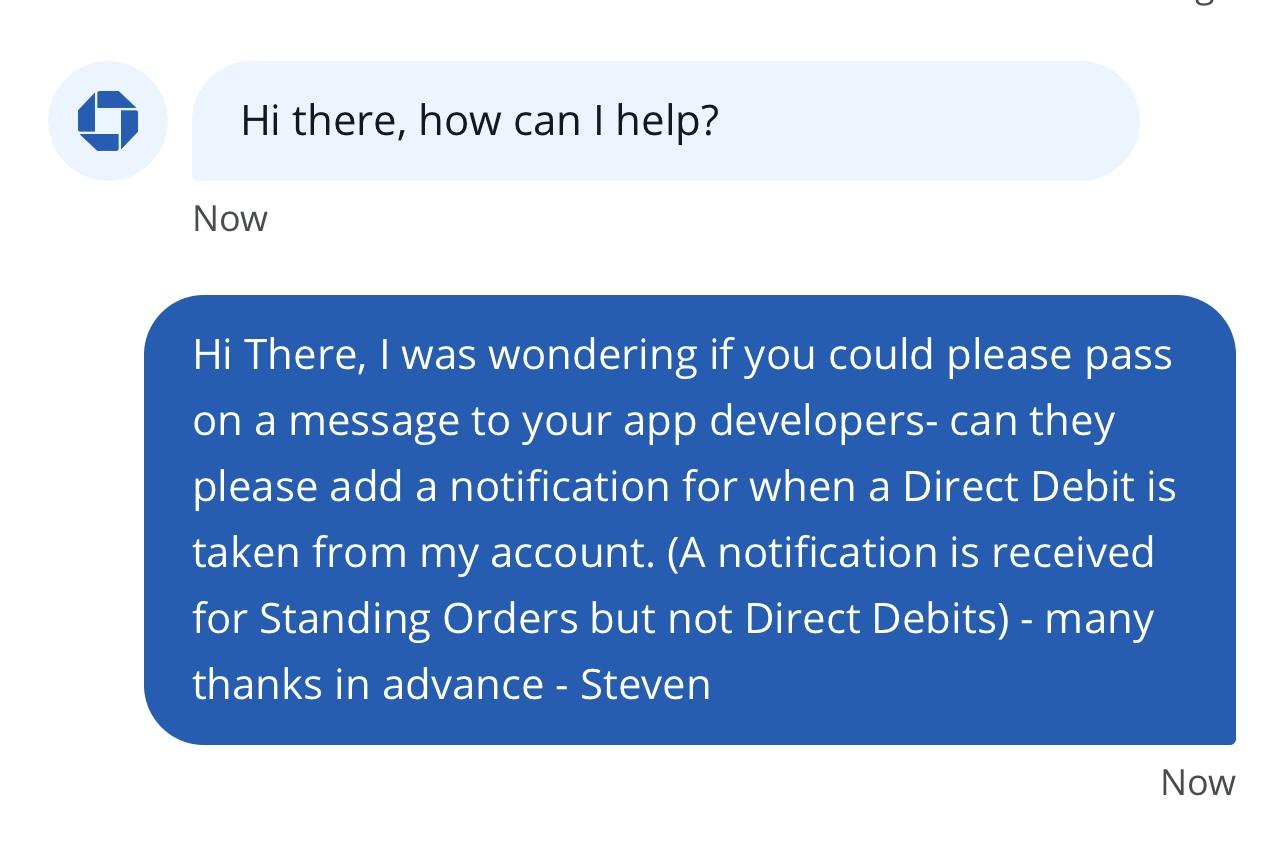

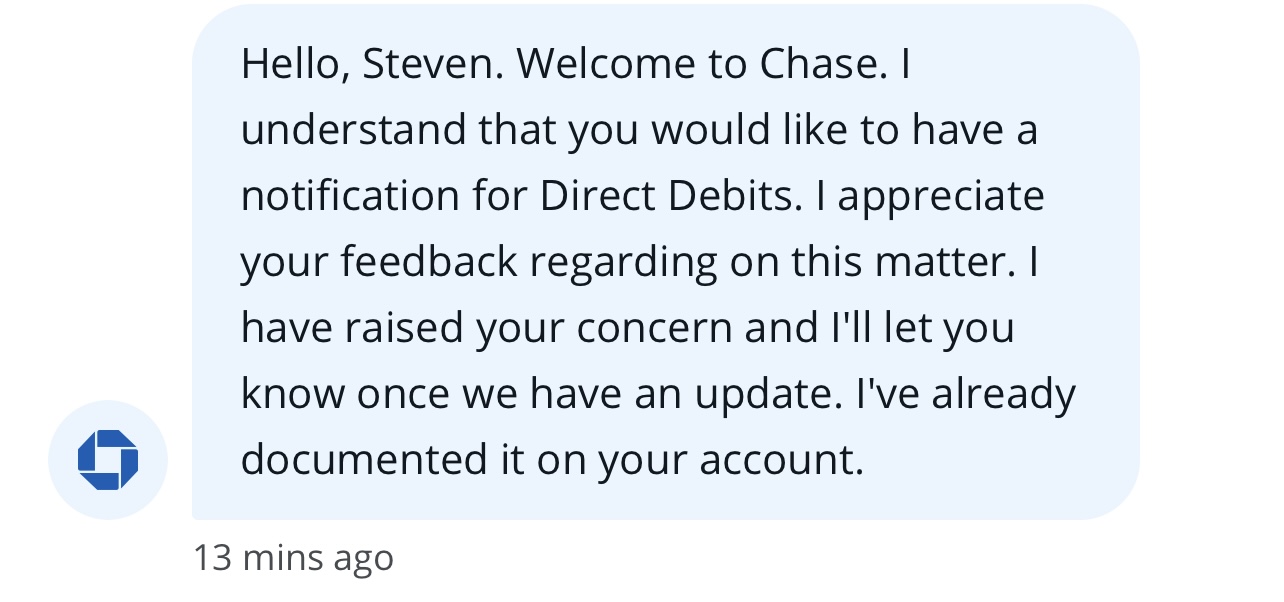

Unfortunately, no notifications for Direct Debits leaving my account this morning but I have raised it with support and we’ll see what happens.

I have to say anything I’ve raised in the past, from alert tones, upcoming payments notification etc have been actioned upon…and like magic we have it…