Yep, here’s the link:

Monzo didn’t get enough votes to make the cut. They scored 82% though which would have placed them fifth between Santander and Nationwide.

Yep, here’s the link:

Monzo didn’t get enough votes to make the cut. They scored 82% though which would have placed them fifth between Santander and Nationwide.

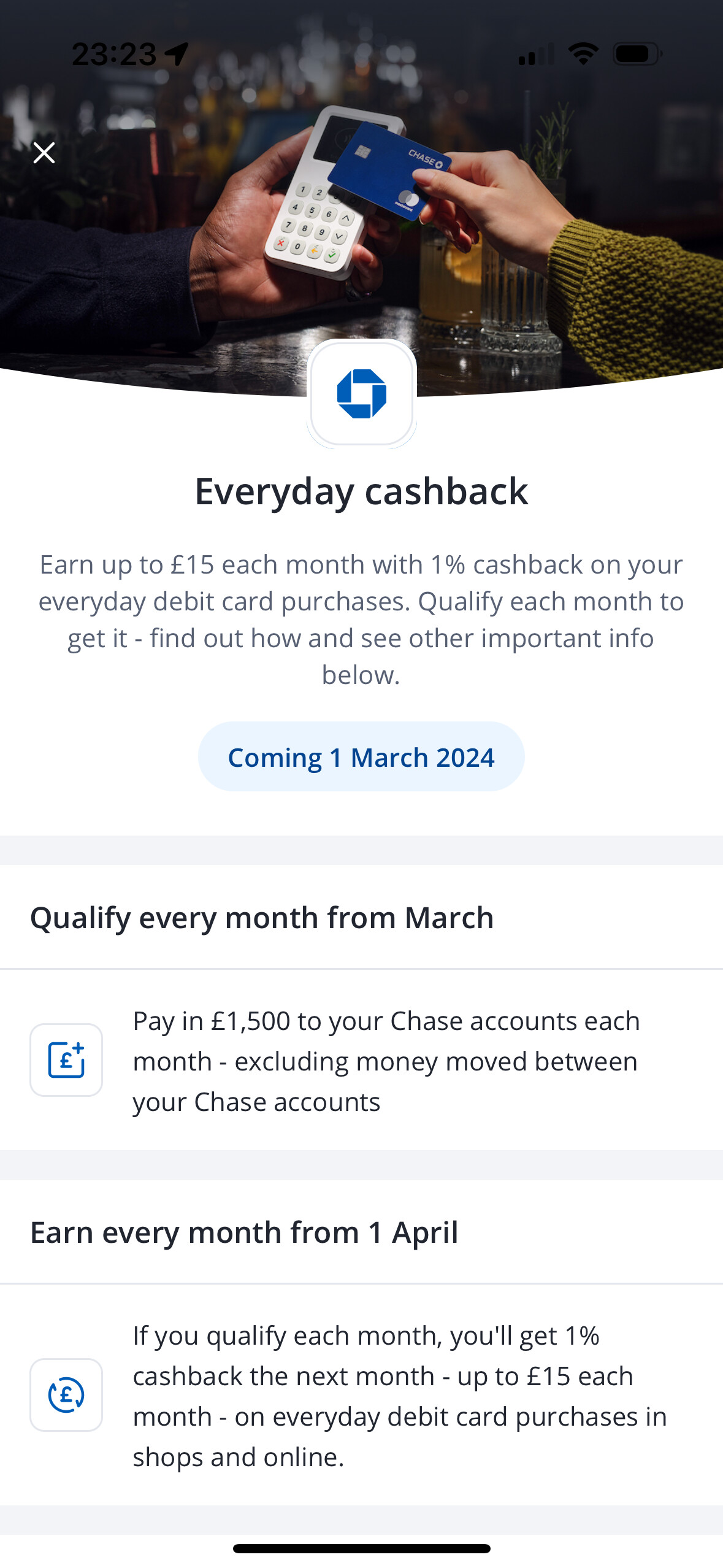

The new cashback offer has gone live in the app. Starts March 1st.

Only differences in the end it turns out are a higher pay in requirement and no fixed end date to the offer. No direct debits. No higher limit on what you can earn. I wonder if they changed things last minute (not out of the question given the recession news a few weeks ago), or if the loose-lipped support agents were misinformed.

A good question.

Can you point me towards that article please? (I can’t locate on their website).

It’s not an article, it’s in the app, in the Rewards section.

The other key difference is that the rumours around the new plan included an increase to £25 a month. Not so, it appears.

Good chance it’s that.

Plus you can pay the money into a savings account rather than needing to put it into a current account first. Minor monthly hassle removed ![]()

Happy that I didn’t have to move direct debits from savings accounts to Current account

Like many, where accounts require a minimum deposit/s in order to access an offer, such as Chase with their £1500pm for the cashback offer, I ping the money in and out of the required account within minutes.

Thankfully, Chase do not appear to have invoked the same clause that I have just seen in the NatWest Switch offer “The deposit of £1,250 can be made up of multiple credits and must remain in the account for 24 hours.”

I wonder how many will fall foul of this and not leave the money in the account long enough ![]()

As I say, something we do not appear to have to worry about with Chase . . . . yet!

I don’t think it’s viable as a monthly condition, personally. I’m not really too sure why Natwest Group have added it as a switch bonus condition either, I think it’s possibly to cover off a hole in the logic they use to check the conditions have been met.

I think they still use outdated systems that may not credit the amount same day depending on the time you send it in though it may be there and usable.

Edit: There’s this weird thing with LBG where I make transfers in or out on weekends but they show a date for Monday or next working day if Monday is bank holiday.

Yes, that is exactly the sort of thing I think they might be trying to workaround.

I agree.

For example, I get paid on the first of the month.

Income enters my account at 01:00

By the time I wake up, 87% of that money has moved, through SO or DD.

The remaining 13% is then moved manually by me that morning.

Yes - also there’s the slightly less extreme case of a weekly paid worker who spend most of their wages every payday on groceries etc.

Chase are changing their savings account interest rate to track the Bank of England rate at 1.15% below.

Wonder why they’re doing that, to be honest. What happens if we go back to ballooning asset prices and 0 interest rates, will we get a negative? (Doubt). No idea why Kroo et al want tracker rates.

No, it won’t go into a negative per the terms changes.

I imagine this is to pre-empt the beginning of the rate starting to fall come next week. I imagine it’s something that’ll be reviewed long before we ever get (if ever, hopefully never) back to a point where the base rate was as good as nothing.

In what way? Having the logo or having the category displayed?

As in merchant information starting to get outdated

Yeah, now that you have edited your OP, I see what you mean ![]()